The Spirax-Sarco Way: Deconstructing the M&A Playbook of a FTSE 100 Serial Acquirer

In the high-stakes world of mergers and acquisitions, the term “serial acquirer” often conjures images of aggressive conglomerates, sprawling private equity firms, or tech giants gobbling up startups. These players dominate headlines with mega-deals and dramatic integration sagas. Yet, some of the most successful practitioners of programmatic M&A operate with a quiet, methodical precision that rarely captures the spotlight. They build empires not through revolutionary disruption, but through disciplined, incremental evolution. Today, we turn our analytical lens on one such master of the craft: Spirax-Sarco Engineering plc. This FTSE 100 stalwart offers a compelling case study in how a long-term vision, deep sector expertise, and a uniquely patient approach to integration can create compounding value over decades. For M&A professionals accustomed to the cut and thrust of rapid-fire deal-making, the Spirax-Sarco way is a lesson in strategic patience and focused execution.

An Introduction to a Quiet Giant

To understand Spirax-Sarco’s M&A strategy, one must first understand the company itself. Founded in 1888, Spirax-Sarco Engineering is a British industrial engineering group with its headquarters nestled in Cheltenham, UK. At its core, the company is a thermal energy management and fluid technology solutions specialist. While managing steam, controlling industrial fluids, and engineering electric heating elements may sound decidedly un-glamorous compared to enterprise software or biotech, these functions are the lifeblood of countless industries, from food and beverage production to pharmaceuticals and power generation. Spirax-Sarco has built a global empire by being the undisputed expert in these critical, niche markets.

The group operates through three distinct but synergistic business segments:

- Steam Specialties: The original and most famous part of the business, providing products and systems for the control and efficient use of steam.

- Electric Thermal Solutions (ETS): A newer but rapidly growing segment focused on advanced electrical heating and temperature management solutions.

- Watson-Marlow Fluid Technology Solutions (WMFTS): A world leader in peristaltic pumps and associated fluid path technologies, primarily serving the pharmaceutical, biotech, and food industries.

Spirax-Sarco’s operational footprint is truly global, demonstrating its strategy of being physically close to its customers. The company maintains direct operations in over 60 countries and sells its products in approximately 130 countries worldwide. It operates a vast network of more than 100 manufacturing plants, service centers, and strategically located offices across the Americas, Europe, the Middle East, Africa, and the Asia-Pacific region. This extensive physical presence is not merely a logistical network; it is a competitive moat, enabling the company to provide the high-touch service, application engineering, and rapid support its customers require.

A History Forged Through Acquisition

Spirax-Sarco’s long history is punctuated by a steady cadence of strategic acquisitions that have shaped the very fabric of the group. Rather than pursuing transformative, “bet-the-company” mergers, its approach has been overwhelmingly focused on acquiring strong, complementary businesses that either bolster an existing capability or provide a foothold in an adjacent, high-growth niche. This disciplined strategy has allowed Spirax-Sarco to evolve from a steam-focused specialist into a diversified thermal and fluid management powerhouse.

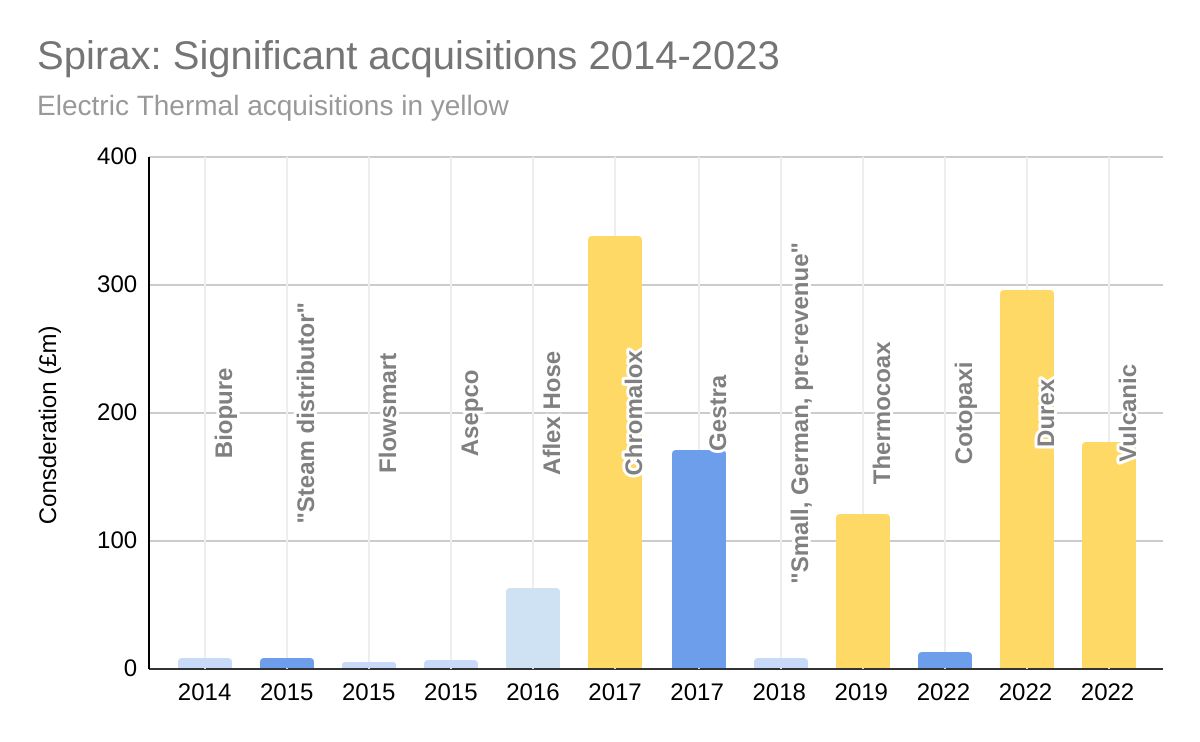

The most significant acquisition in the company’s recent history was the 2017 purchase of Chromalox, a US-based provider of electric thermal technologies, for a staggering £316 million. This deal was swiftly followed by the acquisition of Thermocoax, a key supplier of critical heating components. Together, these acquisitions formed the foundation of the Electric Thermal Solutions (ETS) business segment. This was a pivotal moment, representing a deliberate and sizable strategic pivot towards the global trend of industrial electrification and decarbonization. It was not a random act of diversification but a calculated move into a market directly adjacent to its core thermal expertise.

Looking at a more recent timeframe, Spirax-Sarco’s acquisitive pace remains robust. In the last five years, the company has made several notable purchases, including the acquisitions of Vulcanic and Durex Industries. Vulcanic, a European leader in industrial electric heating, was acquired for €262 million, significantly expanding the ETS segment’s scale and geographic reach in Europe. Durex Industries, a US-based specialist in custom electric thermal solutions, further deepened its technological capabilities in North America.

A clear trend emerges when analyzing these acquisitions. Spirax-Sarco consistently targets companies that are:

- Market Leaders: It buys businesses that are already number one or two in their specific niche.

- Technologically Differentiated: The targets possess unique intellectual property, proprietary technology, or deep application engineering know-how.

- Culturally Aligned: The companies often share a similar engineering-led, customer-centric culture.

- Strategically Adjacent: They operate in markets that are closely related to Spirax-Sarco’s core competencies, allowing for credible synergies and knowledge sharing.

The overarching trend is an unmistakable push towards sustainability and electrification. By acquiring leading players in electric thermal solutions, Spirax-Sarco is positioning itself as a key enabler of industrial decarbonization. This aligns perfectly with its long-term strategy to help customers improve their energy efficiency and reduce their environmental footprint, a service for which they can command a premium. This strategic alignment ensures that each acquisition is not an isolated event but a deliberate step in a much larger, cohesive plan.

The Mechanics of the Deal: Acquisition Methods

For seasoned M&A professionals, the “how” of a deal is just as important as the “what” and “why.” Spirax-Sarco’s approach to structuring and financing its acquisitions is as disciplined and conservative as its target selection. The company typically acquires 100% of its targets, preferring full ownership and control to joint ventures or minority stakes. This allows for cleaner integration and unambiguous strategic direction.

In terms of financing, Spirax-Sarco leverages its strong balance sheet and consistent cash generation. Smaller, bolt-on acquisitions are often funded entirely from existing cash reserves and operational cash flow. This self-funding capability provides significant agility, allowing the company to move quickly and decisively when the right opportunity arises without being beholden to the whims of the capital markets. For larger, more transformative acquisitions like Chromalox or Vulcanic, the company employs a prudent mix of cash and debt. It maintains committed revolving credit facilities with a syndicate of relationship banks, which can be drawn upon to finance these larger transactions. Following a major debt-financed acquisition, the company’s management publicly communicates a clear deleveraging plan, outlining a target net debt-to-EBITDA ratio and a timeline to achieve it, typically within 18 to 24 months. This transparent and credible approach provides reassurance to investors and credit rating agencies, maintaining the company’s financial stability and access to capital.

When it comes to advisory services, Spirax-Sarco does not appear to have a single, exclusively preferred financial advisor. Instead, it maintains strong relationships with a roster of top-tier global and boutique investment banks. Deal announcements over the years have shown collaboration with firms like Rothschild & Co, J.P. Morgan, and others, depending on the geography, size, and specifics of the transaction. This suggests a sophisticated “best-of-breed” approach, where the company selects the advisor best suited for the particular deal at hand rather than relying on a single retainer relationship. The legal and due diligence work is similarly conducted by a select group of leading international law firms and Big Four accounting firms, ensuring a rigorous and comprehensive evaluation process for every transaction.

The Art of the Handshake: Post-Merger Integration Approach

Herein lies what is perhaps the most distinctive and critical element of the Spirax-Sarco M&A playbook: its post-merger integration (PMI) philosophy. While many acquirers pursue an aggressive, top-down integration model focused on rapidly extracting cost synergies by consolidating functions and imposing the parent company’s systems, Spirax-Sarco practices a far more nuanced, decentralized approach. Their mantra is, in essence, to buy great companies and let them continue to be great.

Spirax-Sarco does not have a large, centralized integration office in the traditional sense. Instead, it operates with a lean central M&A team that oversees the transaction and the initial stages of onboarding. The core principle of their integration is to keep the acquired company’s operational identity, management team, and brand intact. They believe that the value they are acquiring lies in the target’s unique culture, customer relationships, and entrepreneurial spirit—all things that a heavy-handed integration could easily destroy.

The integration process focuses on what they call “the Spirax-Sarco way of operating.” This involves a few key areas:

- Financial Reporting and Governance: The acquired company is brought onto Spirax-Sarco’s robust financial reporting systems and governance standards, ensuring transparency and accountability.

- Health, Safety, and Environment (HSE): The group’s high standards for HSE are implemented across the new business, which is a non-negotiable.

- Strategic Support: Spirax-Sarco provides the acquired management team with access to the group’s global resources, capital for investment in growth, and strategic guidance.

Crucially, they do not force the consolidation of sales forces, the immediate adoption of a group-wide ERP system, or the elimination of the acquired company’s headquarters. Synergies are pursued collaboratively and over time, often focusing on revenue opportunities (e.g., cross-selling through Spirax-Sarco’s global network) rather than aggressive cost-cutting. While external integration advisors from major consulting firms may be engaged for specific, complex workstreams on larger deals, the overall responsibility and execution of the integration plan rests heavily with the leadership of the acquired business, supported by the group. This approach builds trust and empowers the local teams, making them partners in value creation rather than subjects of a corporate takeover.

Knowing When to Fold: A Strategy of Divestiture

An M&A strategy is only as good as its discipline, and that includes the willingness to divest assets that no longer fit. While not all acquisitions perform as expected, a look at Spirax-Sarco’s history reveals a striking scarcity of large-scale, high-profile divestitures. This is not an oversight; it is a testament to the rigor of their initial selection and due diligence process. By focusing on high-quality, market-leading businesses in adjacent markets, the company dramatically reduces the risk of strategic missteps or acquiring a “lemon.”

That being said, the company is not dogmatic. It engages in periodic portfolio reviews to ensure all business units align with its long-term strategic direction and meet its stringent financial return criteria. When a business or product line is deemed non-core or a sub-par performer, Spirax-Sarco has shown it is willing to act. However, these actions are typically smaller, tactical divestitures rather than headline-grabbing exits from failed acquisitions. For example, they might prune a minor product line that has become commoditized or sell a small, non-synergistic business unit that came as part of a larger acquisition package.

The strategic reasoning behind any divestiture is consistently one of portfolio optimization. The goal is to focus management attention and capital on the areas with the highest potential for profitable growth, namely their core steam, ETS, and Watson-Marlow segments. Due to the relatively small scale and infrequency of these divestitures, there isn’t a clear pattern of a single preferred divestiture or carve-out advisor. It is likely they would engage one of their relationship investment banks on a case-by-case basis should a more significant divestment be required. The key takeaway is that Spirax-Sarco’s primary strategy is to buy and hold, nurturing its acquisitions for long-term growth, which makes major divestitures a rarity.

Charting the Future Course: The Next Wave of Acquisitions

Looking ahead, we can expect Spirax-Sarco to continue executing its proven M&A playbook with unwavering discipline. The strategic direction is crystal clear: the company is positioning itself at the heart of the global transition towards a more sustainable and efficient industrial sector. This provides a clear roadmap for the type of acquisition targets they will pursue.

Future acquisitions will almost certainly be concentrated in areas that support this sustainability-driven mission. We can anticipate continued activity in the following domains:

- Electric Thermal Solutions: This will remain a hotbed of M&A. Spirax-Sarco will look for targets that expand its geographic reach (particularly in Asia), broaden its technological capabilities in high-growth areas like power electronics and battery manufacturing, or provide access to new industrial end-markets undergoing electrification.

- Digitalization and IoT: The company will likely seek out businesses with expertise in sensors, controls, and software that can enhance the intelligence of its existing products. Imagine “smart steam traps” that predict their own failures or integrated systems that provide customers with real-time data on their energy consumption and carbon footprint.

- Clean Technologies: As industries look beyond simple electrification, technologies related to green hydrogen, carbon capture, and advanced heat recovery will become increasingly important. Spirax-Sarco may look to acquire early-stage or established players in these fields to build out its portfolio of clean thermal solutions.

- Fluid Path Adjancies: Within the Watson-Marlow segment, acquisitions will likely focus on single-use technologies, advanced filtration, and other critical components for the biopharmaceutical and life sciences industries, which continue to exhibit strong, non-cyclical growth.

Spirax-Sarco will not be tempted by targets outside these well-defined strategic lanes, no matter how financially attractive they may appear. The company’s future success will depend on its ability to continue identifying, acquiring, and nurturing the niche champions that will help its industrial customers navigate the complex challenges of the 21st century.

The Spirax-Sarco story is a powerful reminder that in the world of M&A, the most effective strategies are not always the loudest. Through a combination of deep market knowledge, financial prudence, and a uniquely patient and respectful approach to integration, this quiet giant has built a formidable and resilient enterprise. Its playbook serves as an invaluable model for any M&A professional seeking to understand how to build lasting value through programmatic acquisitions.

What other “quietly brilliant” serial acquirers do you believe follow a similar, successful playbook, and what can we learn from their methods?

Leave a comment