The Art of the Bolt-On: Deconstructing Bunzl’s Incessant M&A Machine

In the high-stakes theater of mergers and acquisitions, the spotlight invariably finds the mega-deal. We see the dramatic headlines, the colossal valuations, and the clash of corporate titans. Yet, away from this grand stage, a different and arguably more sustainable form of M&A artistry is quietly being perfected. This is the world of the serial acquirer, the corporate strategist who eschews the single “bet the company” transaction in favor of a disciplined, high-frequency, and compounding approach to growth. These firms build empires not with cannonballs, but with a relentless barrage of precisely aimed pellets. Among the masters of this craft, few are as prolific or as instructive as Bunzl plc. To the uninitiated, Bunzl might be one of the largest companies you have never heard of. For the seasoned M&A professional, however, its model offers a masterclass in strategic execution, disciplined capital allocation, and the powerful mechanics of the bolt-on acquisition. This article deconstructs the engine that drives Bunzl, exploring how it has become a paragon of perpetual, acquisition-led growth.

The Quiet Giant of Global Distribution

To understand Bunzl’s M&A strategy, one must first understand the deceptively simple nature of its business. Bunzl is a specialist international distribution and services group, headquartered in London, UK. Founded in 1854 in Bratislava as a haberdashery, its modern form is that of a colossal B2B provider of essential, not-for-resale goods. These are the critical items that businesses need to operate but do not sell to their own customers. Think of the world’s most successful operator of a global ‘odds and ends’ drawer, and you are getting close. Their product categories are vast and vital: food packaging for supermarkets, cleaning and hygiene supplies for hospitals, safety equipment for construction sites, and guest amenities for hotels.

Bunzl operates under a highly decentralized model, with a global footprint that spans over 30 countries across the Americas, Europe, the UK & Ireland, and Asia Pacific. As a FTSE 100 company, its scale is immense, yet it maintains a local feel through a network of regional businesses. These individual operating companies often retain their original branding and local management, functioning with significant autonomy. This structure is not a historical accident; it is the foundational pillar upon which its entire acquisition philosophy is built. Bunzl does not manufacture these products. Instead, it leverages its global procurement scale to source them efficiently, and its local distribution networks to deliver them effectively, providing a crucial link in the supply chain for tens of thousands of customers.

A Compounding History of Acquisition

Bunzl’s acquisition history is less a series of distinct events and more a continuous, flowing river of capital deployment. The company is a true serial acquirer, methodically adding businesses to its portfolio year after year. Since 2004, Bunzl has completed over 200 acquisitions, a staggering number that underscores its commitment to this growth lever. This is not a strategy of opportunism but one of programmatic execution. In the last five full years (2018-2022), the company acquired approximately 65 businesses. In 2023 alone, it announced a further 12 acquisitions, demonstrating that the pace of its deal-making remains unabated.

While Bunzl is known for its high volume of smaller deals, it does occasionally make more substantial moves. One of its largest recent acquisitions was the 2021 purchase of McCordick & Associates in Canada, a leading distributor of personal protective equipment (PPE). This deal was strategically significant as it substantially grew Bunzl’s safety business in the Canadian market. However, even this “large” deal fits perfectly within the company’s established framework. Bunzl typically targets privately-owned, often family-run, businesses that are leaders in a specific product niche or geographic region. These targets are characterized by:

- Fragmented Markets: They operate in sectors with many small-to-medium-sized players, providing a rich hunting ground for consolidation.

- Strong Management: They often have successful and experienced leadership teams that Bunzl can retain post-acquisition.

- Cultural Fit: They possess an entrepreneurial culture that aligns with Bunzl’s decentralized operating model.

- Core Business Alignment: They distribute essential, not-for-resale products that fit neatly into one of Bunzl’s core sectors like foodservice, cleaning & hygiene, safety, or retail supplies.

The overarching strategy is clear. Each acquisition serves as a “bolt-on” to an existing Bunzl platform, either by expanding its geographic reach into an adjacent territory or by broadening its product offering to the same customer base. A recent trend shows an increasing focus on the safety and hygiene sectors, which offer higher margins and are less susceptible to economic downturns compared to more cyclical areas like retail. This disciplined, compounding approach allows Bunzl to grow steadily, enter new markets with established players, and generate synergies without the immense risk of a single, transformative merger.

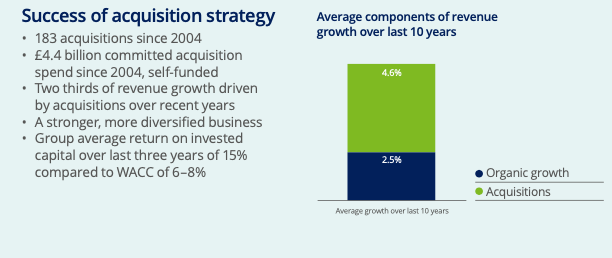

This infographic provides a compelling snapshot of the success behind Bunzl’s acquisition strategy, visually demonstrating that acquisitions are the company’s primary growth engine. The chart clearly breaks down the last decade of revenue growth, showing that acquisitions contributed an average of 4.6% annually, significantly outpacing the 2.5% from organic growth. This powerful visual is backed by impressive statistics detailed on the left, including over 183 self-funded deals since 2004 and a return on invested capital that substantially exceeds the company’s cost of capital, underscoring the effectiveness and financial discipline of their serial acquirer model.

The Mechanics of the Deal Machine

How does a company maintain such a remarkable deal velocity? The answer lies in a finely tuned internal machine rather than a reliance on external advisors for every transaction. While many large corporations engage investment banks for deal sourcing and execution, Bunzl has cultivated a powerful, in-house corporate development function. This dedicated team operates globally, constantly scanning markets, building relationships with business owners, and maintaining an evergreen pipeline of potential targets. They are not just analysts; they are relationship managers who may cultivate a connection with a target company’s founder for years before a deal ever materializes. This proactive, relationship-based sourcing gives Bunzl a significant competitive advantage, allowing it to often engage in proprietary, off-market negotiations, avoiding competitive auction processes that can drive up multiples.

When it comes to financing, Bunzl’s method is a testament to its financial prudence and operational strength. The vast majority of its acquisitions are funded through its own cash flow and existing debt facilities. The company generates substantial, reliable free cash flow from its operations, which it then recycles into new acquisitions. This self-funding model provides tremendous agility. It means Bunzl can move quickly and decisively when an opportunity arises, without the delays and complexities associated with raising external equity or securing deal-specific debt financing. For a seller, the certainty of a cash-rich buyer like Bunzl is a highly attractive proposition. While the company maintains relationships with a panel of banks for its main credit facilities, it does not appear to have a single preferred financial advisor that it uses for all its M&A transactions. The sheer volume and smaller average size of its deals make an in-house model far more efficient and cost-effective.

Integrating Without Obliterating: The Bunzl PMI Model

Post-merger integration (PMI) is often cited as the reef upon which many well-intentioned acquisitions founder. Here, again, Bunzl diverges from the conventional playbook. The classic PMI approach involves deep, top-down integration, consolidating everything from IT systems and HR policies to sales teams and operational headquarters in a relentless pursuit of cost synergies. Bunzl’s approach is fundamentally different and is best described as “integration-light.” The company does not have a large, centralized integration office in the traditional sense. Instead, the responsibility for integration rests with the leadership of the regional Bunzl platform to which the new company is being bolted.

The core of Bunzl’s PMI philosophy is to preserve the very things that made the acquired company successful in the first place: its local market knowledge, its customer relationships, and its entrepreneurial spirit. The existing management team is almost always retained and empowered to continue running the day-to-day business with a high degree of autonomy. Bunzl’s integration focuses on a few key areas where its scale provides immediate value:

- Financial Reporting: The acquired company is plugged into Bunzl’s financial reporting and control systems for oversight and transparency.

- Procurement Synergies: The new business gains access to Bunzl’s global sourcing power, often enabling it to purchase products at a lower cost and improve its margins.

- Best Practices: Knowledge and best practices from across the global Bunzl network are shared, but not dogmatically imposed.

This decentralized, trust-based model is a powerful selling point to founders who wish to see their legacy continue and are not ready to retire. They can de-risk their personal financial position by selling to a stable, global leader while continuing to run the business they built. This approach minimizes the cultural clashes and operational disruptions that plague more aggressive integrations, ensuring a smoother transition and a faster path to value realization. While Bunzl may leverage external specialists for specific due diligence streams like tax or environmental assessments, the core strategic and operational integration is an internally managed process, guided by its foundational decentralized ethos.

Pruning the Portfolio: The Logic of Strategic Divestitures

No acquirer, no matter how skilled, has a perfect track record, and market dynamics invariably shift over time. An essential, though less celebrated, component of a mature M&A strategy is the discipline to divest assets that no longer fit the strategic vision. Bunzl is no exception. While its primary focus is on accumulation, the company is an active portfolio manager and is not afraid to prune its holdings when necessary. Divestitures are undertaken when a business is deemed non-core, operates in a market with diminishing growth or margin prospects, or faces headwinds that divert management attention from more promising areas.

The most significant recent example was the 2019 divestiture of its UK healthcare business, which supplied goods to the National Health Service (NHS). This was followed by the sale of other smaller, non-core marketing and retail businesses. The strategic reasoning was multifaceted. These businesses were often characterized by lower margins and more challenging market structures compared to Bunzl’s preferred B2B distribution niches. For instance, the UK healthcare supplies market involved centralized, powerful buyers and intense pricing pressure. By divesting these assets, Bunzl was able to sharpen its focus on higher-margin, higher-growth sectors like safety, foodservice, and cleaning & hygiene. This move also freed up both capital and management bandwidth to be redeployed into acquisitions that better aligned with its long-term strategy. Just as with acquisitions, Bunzl does not appear to have a single, preferred carve-out advisor, likely handling smaller divestitures internally and engaging specialist firms on a case-by-case basis for more complex transactions that require intricate separation planning.

The Road Ahead: What’s Next for the Bunzl Engine?

Looking to the future, there is little reason to expect Bunzl’s acquisition engine to slow down. The company’s core strategy is proven, resilient, and perfectly suited to the current global landscape. The markets in which it operates remain highly fragmented, offering a long runway for continued consolidation. Expect the company to continue its disciplined hunt for high-quality, privately-owned distributors across its key geographies and sectors. We can anticipate a continued emphasis on targets in the safety and hygiene categories, as these markets benefit from long-term structural tailwinds related to increased regulation and a greater societal focus on health and wellness.

Furthermore, sustainability will likely become an even more critical lens for target selection. Bunzl will increasingly look for businesses that specialize in eco-friendly packaging, sustainable cleaning products, and other solutions that help its customers meet their own ESG goals. The company may also look to make small, strategic entries into new, adjacent product categories or geographies where it can establish a new platform for future bolt-on acquisitions. The beauty of the Bunzl model is its scalability and repeatability. The pipeline is perpetually refreshed, the financing is readily available from internal resources, and the integration model is designed for minimal disruption. The machine is built to run continuously.

In conclusion, Bunzl represents a powerful counter-narrative to the headline-grabbing mega-deal. Its success is a testament to the virtues of discipline, focus, and the compounding power of a high-volume, bolt-on acquisition strategy. By perfecting a repeatable process for sourcing, executing, and lightly integrating smaller businesses, it has built a global powerhouse one deal at a time. The model is less about a single grand design and more about the masterful assembly of a thousand carefully chosen parts. As the M&A landscape continues to evolve amidst economic uncertainty and shifting capital markets, is Bunzl’s decentralized, high-volume model the most resilient strategy for long-term value creation, or does its ever-expanding complexity present a hidden, future risk?

Leave a comment