Splitting to Succeed: How the Comm-Co / Op-Co Structure Unlocks Value in Corporate Spin-Offs

In the high-stakes theater of corporate strategy, the spin-off has long been a star performer. The act of carving out a business unit into a new, independent entity can unlock value, sharpen focus, and appease restless shareholders. However, as M&A professionals know, the success of the separation lies not just in the decision to split, but in the architectural elegance of the split itself. A particularly sophisticated and increasingly relevant design is the “Comm-Co / Op-Co” structure. This model moves beyond a simple divestiture, creating a symbiotic relationship between two distinct entities that can optimize everything from asset management to operational agility. For the seasoned dealmaker, understanding this structure is no longer a niche specialty; it is a critical tool for crafting transactions that deliver durable, long-term value. This article will dissect the Comm-Co / Op-Co framework, explore its core value propositions, and examine real-world examples to provide a clear playbook for its application in global M&A.

Demystifying the Jargon: Core Concepts and Context

Before diving into the strategic application, we must first establish a shared vocabulary and understanding of the foundational elements.

What Exactly Is a “Comm-Co / Op-Co” Structure?

At its heart, the “Commercial Company / Operating Company” structure is a method of corporate organization that separates the ownership of key assets from the business that utilizes those assets. Think of it as a deliberate unbundling of responsibilities into two specialized, yet contractually linked, entities:

- The Commercial Company (Comm-Co): This entity is the asset holding company. It owns the valuable, often capital-intensive or strategic assets. These can include real estate, intellectual property (patents, brands, trademarks), critical infrastructure (pipelines, data centers, cell towers), or long-term supply contracts. The Comm-Co’s primary role is to manage, maintain, and monetize these assets strategically. It functions as the landlord, the patent licensor, or the infrastructure provider.

- The Operating Company (Op-Co): This entity is the engine of the business. It leases or licenses the assets from the Comm-Co to run the day-to-day operations. The Op-Co is the customer-facing business that employs the staff, manages the supply chain, markets the products or services, and drives revenue. Its focus is purely on operational excellence, market competition, and customer satisfaction. It is the tenant running the restaurant, the manufacturer using the patented technology, or the service provider using the infrastructure.

The two are bound by a series of long-term, arm’s-length agreements, such as master lease agreements, licensing agreements, or master service agreements (MSAs). These contracts define the terms of their relationship, including payment structures, service level expectations, and usage rights. It’s the corporate equivalent of deciding that while you love owning the restaurant building, you would rather let a Michelin-starred chef handle the daily chaos of the kitchen.

The Structure in a Spin-Off Context

When applied to a spin-off, this structure takes on a powerful strategic dimension. Instead of spinning off a fully integrated business, a parent company can separate a division’s assets and operations. For example, a large conglomerate spinning off its manufacturing division could place all the factories and proprietary process patents into a new Comm-Co that it retains or also spins to shareholders. Simultaneously, it spins off the operational side—the management team, sales force, and production workforce—as an Op-Co. The new, publicly traded Op-Co then pays the Comm-Co a fee to lease the factories and license the patents. This creates two “pure-play” entities from one, each with a distinct investment thesis.

Why Now? Current Trends Fueling the Model

The rise of the Comm-Co / Op-Co structure is not coincidental. It is a direct response to several powerful market forces. Shareholder activists are relentlessly pushing for companies to unlock “hidden value” trapped within complex, vertically integrated structures. Furthermore, there is a growing premium on business model clarity and focus. Investors increasingly want to invest in either a stable, asset-backed, dividend-paying entity (the Comm-Co) or a high-growth, agile, and capital-light operator (the Op-Co), but not necessarily a muddled combination of both. This trend, combined with the continuous search for tax efficiencies and operational nimbleness in a volatile global economy, has made the Comm-Co / Op-Co split a highly attractive strategic option.

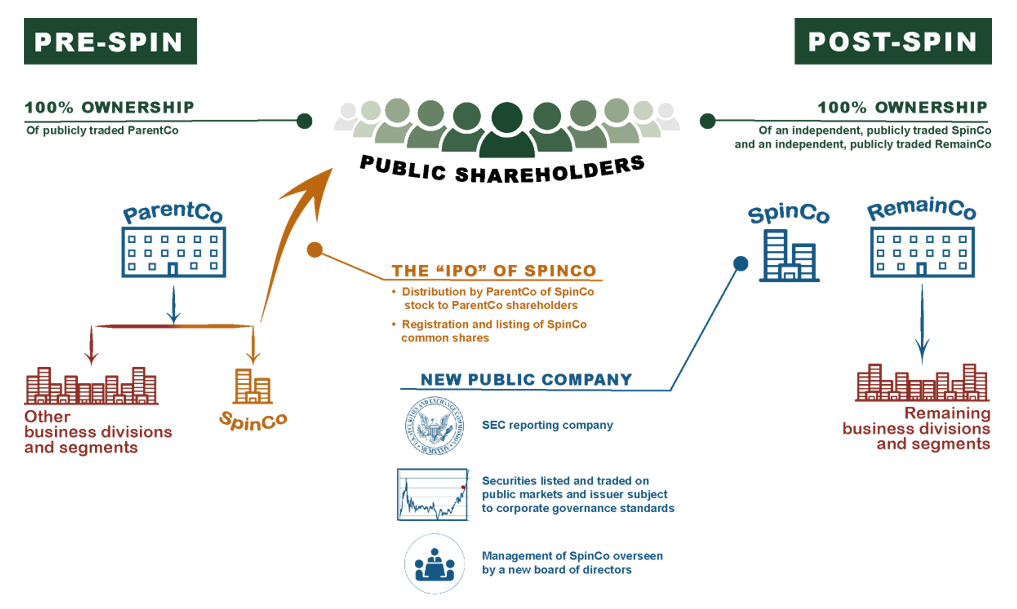

This flow diagram illustrates the ‘before and after’ of a corporate spin-off, showing how a single ParentCo becomes two independent public entities—SpinCo and RemainCo—both owned by the original shareholders. This is the essential transaction underlying the Comm-Co / Op-Co strategy, creating the separate, focused companies discussed in the article.

The Three Pillars of Value Creation

Executing a Comm-Co / Op-Co spin-off is complex, but the strategic rewards are compelling. The value created rests on three distinct but interconnected pillars.

Pillar 1: Strategic Asset Optimization and Risk Mitigation

The most fundamental benefit is the ability to strategically manage assets and insulate them from operational risk. By housing high-value assets like real estate or intellectual property in a separate Comm-Co, a company effectively builds a firewall. The Comm-Co is shielded from the liabilities and cyclicality of the operating business, such as litigation, labor disputes, or market downturns. This concept, known as bankruptcy remoteness, makes the Comm-Co a much more stable and creditworthy entity.

This stability directly enhances its ability to raise capital. Lenders are more willing to provide favorable financing against a clean portfolio of tangible or intangible assets with a predictable revenue stream (the lease or license payments from the Op-Co) than against a complex operating business with myriad risks. The Comm-Co can then use this efficiently raised capital to reinvest in and upgrade its asset base or acquire new assets, creating a virtuous cycle of growth. For the Op-Co, being “asset-light” reduces the capital it needs to tie up in its balance sheet, freeing it to invest in growth initiatives like marketing, R&D, and talent acquisition.

Pillar 2: Enhanced Operational Efficiency and Focus

A well-executed Comm-Co / Op-Co structure fosters a culture of intense focus within each entity. Freed from the burden of long-term asset management, capital-intensive maintenance, and real estate strategy, the Op-Co’s management team can dedicate 100% of its attention to its core purpose: winning in the marketplace. Their key performance indicators are clear: revenue growth, market share, customer satisfaction, and operational efficiency. This singular focus breeds agility, allowing the Op-Co to respond more quickly to changing customer demands and competitive threats.

Conversely, the Comm-Co’s management team develops deep expertise in asset management. Their job is not to run a factory but to maximize the value and yield of a portfolio of factories. They focus on long-term capital planning, preventative maintenance, property acquisitions or disposals, and strategic monetization of intellectual property. This specialization leads to more professional and strategic asset stewardship than is often possible when assets are just one of many responsibilities for an integrated business unit’s leadership. Each company does what it does best, creating a sum that is greater than its parts.

Pillar 3: Unlocking Financial Flexibility and Tailored Investor Appeal

Perhaps the most compelling pillar for M&A professionals is the structure’s ability to unlock valuation multiples by appealing to different investor appetites. A single, integrated company often trades at a blended valuation multiple that fails to fully recognize the value of its distinct parts. Separating the company into a Comm-Co and an Op-Co clarifies the investment thesis for each:

- The Comm-Co becomes a proxy for a real estate investment trust (REIT), an infrastructure fund, or an IP royalty company. It offers stable, predictable, long-term cash flows from its contractual agreements with the Op-Co. This profile is highly attractive to income-oriented investors, such as pension funds, insurance companies, and sovereign wealth funds, who are willing to pay a high multiple for predictable yield.

- The Op-Co becomes a classic “pure-play” operator. As an asset-light business with high operating leverage, its value is tied to its growth potential, brand strength, and operational execution. This profile appeals to growth-oriented investors, including private equity firms and public equity growth funds, who are willing to pay a premium for a scalable business model with a high return on invested capital (ROIC).

By creating two distinct securities, the company allows the market to price each one efficiently according to its specific risk and return profile. This de-conglomeration discount is often eliminated, leading to a scenario where the combined market capitalization of the two separate entities is significantly higher than that of the original, integrated firm.

The Structure in Action: Real-World Case Studies

Theory is valuable, but its true test is in its application. Several high-profile corporate separations demonstrate the power of this structural approach.

Case 1: The Real Estate Play – Hilton Worldwide

One of the most classic and clear-cut examples of a Comm-Co / Op-Co strategy is Hilton Worldwide’s 2017 decision to spin off the bulk of its real estate assets. The company executed a complex trifurcation, resulting in three distinct, publicly traded companies:

- Hilton Worldwide Holdings (The Op-Co): The remaining company became a capital-light hotel management and franchising business. It owns the iconic brands (Hilton, Waldorf Astoria, Embassy Suites) and focuses on managing hotels for property owners and selling franchises. Its value is driven by brand equity, operational excellence, and fee-based revenue streams.

- Park Hotels & Resorts (The Comm-Co): This new entity became one of the largest publicly traded lodging REITs. It owns a portfolio of high-end hotels and resorts, which it leases primarily to Hilton to operate. Its value is tied to the quality of its real estate portfolio and the stable, long-term rental income it receives.

- Hilton Grand Vacations (A Hybrid): This third entity was a spin-off of Hilton’s timeshare business, which has its own unique operating and real estate model.

The strategic rationale was textbook. By separating the real estate (Comm-Co) from the brand management (Op-Co), Hilton allowed investors to choose their preferred investment: stable property ownership or a high-growth, asset-light fee business. The market responded by assigning distinct and, in aggregate, higher valuation multiples to the separate parts than it had to the consolidated entity.

Case 2: The Intellectual Property Play – Pfizer and Viatris

The pharmaceutical industry provides fertile ground for Comm-Co / Op-Co logic, with intellectual property (patents) serving as the key asset. A prime example is the formation of Viatris in 2020. This transaction involved Pfizer spinning off its Upjohn division, which managed its portfolio of mature, off-patent branded drugs (like Lipitor and Viagra), and combining it with Mylan, a global generic and specialty pharmaceuticals company.

In this model, one can view the combined Viatris as a type of Comm-Co/Op-Co hybrid. It manages a massive portfolio of established pharmaceutical “assets” (the drug formulations and brands) and focuses on optimizing their commercialization and manufacturing efficiency on a global scale. This move allowed the remaining Pfizer (the “innovator”) to sharpen its focus and capital allocation exclusively on its high-risk, high-reward pipeline of innovative, patent-protected medicines and vaccines. The separation allowed investors to choose between a high-growth, R&D-driven innovator (Pfizer) and a high-volume, value-and-dividend-focused global generics powerhouse (Viatris).

Case 3: The Infrastructure Play – DTE Energy and DT Midstream

The energy sector, with its heavy infrastructure assets, is another natural fit for this structure. In 2021, DTE Energy, a diversified energy company based in Detroit, completed the spin-off of its non-utility natural gas pipeline, storage, and gathering business, creating a new, independent company called DT Midstream.

- DTE Energy (The Regulated Op-Co): The parent company became a more “pure-play” regulated electric and natural gas utility. Its primary focus is on serving its customers, investing in the grid, and navigating the state regulatory environment to earn a stable, predictable rate of return.

- DT Midstream (The Infrastructure Comm-Co): The new spin-off became an asset-heavy company that owns and operates a network of valuable gas pipelines and storage facilities. Its business is to provide transportation and storage services to a variety of customers under long-term, fee-based contracts, generating predictable cash flows characteristic of an infrastructure asset owner.

This separation provided investors with greater clarity. Those seeking the safety and dividend yield of a regulated utility could invest in DTE. Those seeking exposure to the growth of natural gas infrastructure, with cash flows backed by long-term contracts, could invest in DT Midstream. The move was designed to unlock a higher valuation for the midstream assets, which were previously undervalued within the larger, more complex utility holding company structure.

A Practical Framework and a Word of Caution

While the benefits are clear, implementing a Comm-Co / Op-Co spin-off is a formidable undertaking that requires meticulous planning and execution.

A Practical Framework: Setting Up the Structure

Successfully navigating this process typically involves several critical steps:

- Asset Identification and Segregation: The first step is a rigorous analysis to identify which assets will move to the Comm-Co and which will remain with the Op-Co. This requires clear criteria and can be contentious, involving legal, tax, and operational teams.

- Legal Entity Creation and Capitalization: This involves the legal work of forming the new entities, defining their corporate charters, and establishing their initial balance sheets and capital structures.

- Crafting the Intercompany Agreements: This is arguably the most crucial step. Lawyers and business leaders must draft ironclad, arm’s-length agreements (leases, licenses, MSAs) that govern the relationship. These documents must clearly define pricing, service levels, duration, and dispute resolution mechanisms.

- Governance and Management: Independent boards and management teams must be appointed for each entity. Defining clear governance protocols is essential to manage the inherent interdependencies and potential for conflicts of interest.

- Tax and Regulatory Planning: The entire transaction must be structured to be as tax-efficient as possible (e.g., qualifying as a tax-free spin-off in the U.S. under Section 355). It also requires navigating a maze of regulatory, accounting, and stock exchange requirements.

A Word of Caution: Potential Drawbacks and Complexities

This structure is not a panacea. The interdependency between the Comm-Co and Op-Co can create significant challenges. A struggling Op-Co could default on its payments, placing the Comm-Co’s revenue stream at risk. Conversely, an inflexible or demanding Comm-Co could hamstring the Op-Co’s ability to adapt to market changes. Transfer pricing—the price at which the entities transact—is a major area of scrutiny from tax authorities, who tend to view complex intercompany agreements with the same cheerful enthusiasm as a cat views a bath. Finally, there is the risk of creating a “hollowed out” Op-Co, so dependent on its former parent that it struggles to innovate or stand on its own.

The Future of Corporate Architecture?

The Comm-Co / Op-Co structure represents a sophisticated evolution in corporate design. It is a powerful response to the market’s demand for focus, clarity, and efficient capital allocation. By surgically separating asset ownership from operations, companies can unlock valuation multiples, enhance operational focus, and create tailored investment vehicles that appeal to a broader and more discerning investor base. While the path to implementation is fraught with complexity and requires nuanced judgment, the strategic rewards can be transformative. It is a testament to the idea that sometimes, the best way to grow together is to first split apart.

As we look ahead, the pressures of shareholder activism, intense competition, and the relentless pursuit of efficiency are unlikely to wane. This leads to a fundamental question for the future of corporate strategy. In an era of relentless specialization, is the fully integrated conglomerate model becoming a relic, and is this structural separation the default path forward for unlocking value?

Leave a comment