Assa Abloy: How the World’s Largest Lock Company Built an Empire One Acquisition at a Time

In the world of serial acquirers, a handful of names surface repeatedly in boardroom conversations and M&A textbooks: Danaher, Constellation Software, Illinois Tool Works. Yet one Scandinavian powerhouse has quietly assembled a portfolio of over 300 acquisitions across four decades, locking down global leadership in an industry most dealmakers rarely think about until they reach for a door handle. Assa Abloy, the Swedish access solutions giant, has executed one of the most disciplined and sustained acquisition programs in modern corporate history, transforming a fragmented market of regional lock and hardware manufacturers into a cohesive, technology-driven platform spanning every inhabited continent.

For M&A professionals, Assa Abloy offers a masterclass in how to use acquisitions not merely as a growth lever but as a strategic architecture—one that integrates hardware legacy with digital transformation, balances bolt-on deals with transformative bets, and manages post-merger integration at a cadence that would exhaust most corporate development teams. This article examines the company’s acquisition history, methods, integration philosophy, divestiture discipline, and likely future trajectory. The aim is to give practitioners a granular understanding of what makes Assa Abloy’s acquisition engine function—and what lessons it holds for serial acquirers operating in any sector.

Who Is Assa Abloy?

Assa Abloy was formed in 1994 through the merger of the Swedish lock manufacturer Assa and the Finnish lock group Abloy. The combination was orchestrated by Investment AB Latour and the Finnish conglomerate Wärtsilä, both of which recognized that the global lock and security industry was ripe for consolidation. The merged entity established its headquarters in Stockholm, Sweden, where it remains today, and listed on the Nasdaq Stockholm exchange.

The company operates in the access solutions sector, which encompasses mechanical locks, electromechanical locks, digital door locks, access control systems, identification technology, entrance automation, and hotel security systems. In practical terms, Assa Abloy manufactures and sells the products that control who enters and exits buildings, rooms, gates, and digital perimeters around the world. Its brand portfolio includes globally recognized names such as Yale, HID Global, Mul-T-Lock, August (smart locks), and dozens of regional champions.

Assa Abloy organizes its operations into three principal divisions: EMEIA (Europe, Middle East, India, and Africa), Americas, and Asia Pacific. A fourth segment, Global Technologies, houses the company’s digital access and identification businesses, including HID Global. The company employs approximately 52,000 people across more than 70 countries. It maintains production facilities in Sweden, Finland, the United States, Mexico, China, India, Romania, the Czech Republic, and numerous other locations—a manufacturing footprint that mirrors its acquisition footprint almost precisely. Assa Abloy generated revenues of approximately SEK 133 billion (roughly USD 12.5 billion) in 2023, making it the undisputed global leader in access solutions by a wide margin over competitors such as Allegion, Dormakaba, and Spectrum Brands’ hardware division.

Understanding the breadth of Assa Abloy’s operational geography matters for any analysis of its acquisition strategy. The company does not acquire in a vacuum. Each deal slots into a regional or technological matrix, and the global manufacturing network provides the integration infrastructure that makes high acquisition velocity sustainable.

Acquisition History: More Than 300 Deals and Counting

Assa Abloy’s acquisition history is central to its identity. From the moment of its founding merger in 1994, the company was conceived as a consolidation vehicle. Carl-Henric Svensson, the company’s first CEO, and his successor Bo Dankis established the acquisition playbook in the late 1990s, rapidly absorling regional lock manufacturers across Europe and North America. Under the tenure of Johan Molin, who served as CEO from 2005 to 2023, the company accelerated and diversified its acquisition program dramatically, expanding into electromechanical solutions, access control software, mobile credentials, and entrance automation. Nico Delvaux assumed the CEO role in 2023 and has maintained the acquisition cadence.

Since its formation, Assa Abloy has completed over 300 acquisitions. The company routinely closes between 10 and 20 transactions per year, a pace that has held remarkably steady across economic cycles. In the five-year period from 2019 through 2023, Assa Abloy completed approximately 60 to 70 acquisitions, though the exact count varies depending on whether one includes smaller asset purchases and minority stake increases. In 2023 alone, the company closed roughly a dozen transactions, a number consistent with its long-term average when adjusting for the temporary distraction of regulatory proceedings related to its largest-ever attempted deal.

That deal—the proposed acquisition of the Hardware and Home Improvement (HHI) division of Spectrum Brands—deserves special attention. Announced in September 2021 for an enterprise value of approximately USD 4.3 billion, the HHI transaction would have been Assa Abloy’s largest acquisition by a considerable margin. HHI’s portfolio included the Kwikset and Baldwin lock brands, which dominate the U.S. residential market. However, the U.S. Department of Justice filed suit to block the deal in September 2022, citing concerns about reduced competition in the residential door hardware market. Assa Abloy proposed divestitures to satisfy regulators, and after protracted litigation, the parties ultimately abandoned the transaction in mid-2024 following an unfavorable court ruling. The failed HHI bid stands as a significant strategic setback, not because it threatened Assa Abloy’s financial health, but because it highlighted the limits that antitrust enforcement increasingly places on dominant acquirers seeking further consolidation in concentrated markets.

Setting aside the HHI episode, Assa Abloy’s largest completed acquisition remains its 2011 purchase of Cardo’s entrance automation division for approximately SEK 8.4 billion. That deal moved the company decisively into automatic doors, pedestrian entrances, and loading dock solutions—a segment now contributing significantly to group revenues and representing one of Assa Abloy’s highest-growth areas.

The types of companies Assa Abloy acquires fall into several discernible categories:

- Regional mechanical lock manufacturers: These were the bread-and-butter acquisitions of the company’s early years and continue as bolt-on deals in emerging markets across Africa, Southeast Asia, and Latin America. They expand geographic coverage and consolidate fragmented local markets.

- Electromechanical and digital access companies: As the industry has migrated from purely mechanical products to connected, software-enabled solutions, Assa Abloy has systematically acquired companies offering electronic locks, biometric readers, mobile access credentials, and cloud-based access management platforms.

- Entrance automation businesses: Following the Cardo acquisition, the company has continued to bolt on automatic door and industrial entrance manufacturers, building scale in a segment with attractive aftermarket revenue profiles.

- Identification and credentialing technology firms: Through HID Global, Assa Abloy has acquired companies specializing in secure identity solutions, including card printing, physical access credentials, and citizen ID platforms used by governments.

The trend line across these categories is unmistakable. Assa Abloy is systematically shifting its portfolio toward higher-technology, higher-margin, recurring-revenue business models. Mechanical locks, while still a substantial revenue contributor, are a declining share of the mix. Digital and electromechanical solutions, entrance automation, and identity technology represent the company’s future—and its acquisition pipeline reflects that prioritization.

This strategic alignment between acquisition targeting and corporate strategy is not accidental. Assa Abloy articulates a clear framework in its annual reports: the company seeks to strengthen its position as the global leader in access solutions by acquiring businesses that either expand its geographic reach in underpenetrated markets or advance its technology capabilities along the analog-to-digital continuum. Every acquisition, in theory, must satisfy at least one of those two criteria.

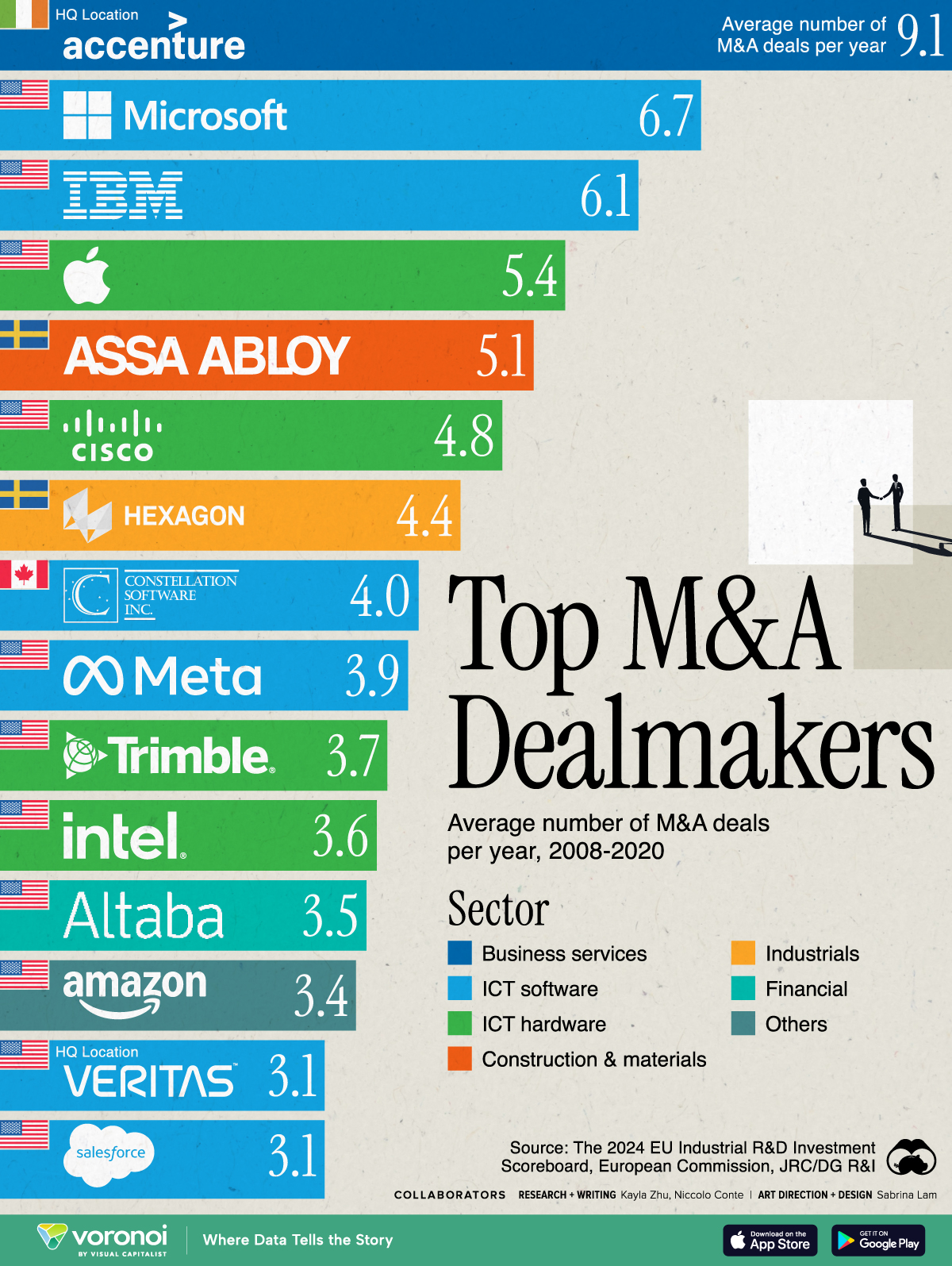

Top M&A Dealmakers by average number of deals per year (2008–2020): Assa Abloy ranks fourth globally with an average of 5.1 acquisitions per year, placing the Swedish industrials company alongside tech giants like Microsoft, IBM, and Apple as one of the world’s most active serial acquirers.

Acquisition Methods: Financing, Advisors, and Deal Execution

Assa Abloy’s acquisition methodology reflects its Scandinavian roots: disciplined, process-driven, and not given to dramatic flourishes. The company’s corporate development function operates as a well-oiled pipeline rather than a sporadic deal machine. Deal sourcing combines proactive identification of targets with inbound opportunities flowing from the company’s extensive industry relationships. Division presidents and regional managers play an active role in identifying and championing acquisition candidates, ensuring that strategic fit is assessed by operators who understand the target’s market context, not just by financial analysts running discounted cash flow models.

The majority of Assa Abloy’s acquisitions are privately negotiated transactions. The company acquires predominantly private, often family-owned businesses—a characteristic common to consolidators operating in fragmented industrial markets. Public company acquisitions have been rare, with the attempted HHI deal being a notable exception. Private negotiations allow Assa Abloy to control deal timelines, maintain confidentiality, and avoid auction dynamics that inflate multiples.

From a financing perspective, Assa Abloy funds its acquisitions through a combination of operating cash flow and debt. The company generates robust free cash flow—typically in the range of SEK 15 to 20 billion annually—which provides substantial self-funding capacity for its steady diet of small and mid-sized bolt-on acquisitions. For larger transactions, Assa Abloy taps its committed credit facilities and the investment-grade debt capital markets. The company maintains a BBB+ credit rating from S&P, which it manages carefully, allowing temporary leverage increases for significant deals while committing to rapid deleveraging afterward. Equity financing has not been part of Assa Abloy’s acquisition toolkit in any meaningful way for decades, which reflects management’s preference for preserving shareholder value and avoiding dilution.

Regarding financial advisory relationships, Assa Abloy does not publicly disclose a single preferred advisor, and the evidence suggests that it works with multiple investment banks depending on deal size, geography, and complexity. For larger transactions, the company has engaged bulge-bracket firms. Goldman Sachs, for example, advised Assa Abloy on the HHI acquisition attempt. For mid-market and regional deals, the company likely draws on relationships with Scandinavian banks such as SEB and Handelsbanken, as well as regional M&A boutiques in relevant markets. The company’s corporate development team possesses sufficient in-house capability to execute smaller bolt-on deals with minimal external advisory input, which keeps transaction costs proportionate and maintains institutional knowledge within the organization.

Legal advisory work similarly spans multiple firms, with the company engaging international law firms for cross-border transactions and local counsel for jurisdiction-specific regulatory and contractual matters. The failed HHI transaction, for instance, involved significant litigation counsel in the United States to contest the DOJ’s challenge.

Post-Merger Integration: The Engine Behind the Acquisition Machine

The difference between a successful serial acquirer and a company that merely accumulates businesses lies almost entirely in integration execution. Assa Abloy has recognized this reality from its earliest days and has built a sophisticated, repeatable integration model that scales across dozens of simultaneous integration efforts.

Assa Abloy maintains an internal integration capability embedded within its divisional structure rather than operating a single centralized integration office. Each division—EMEIA, Americas, Asia Pacific, and Global Technologies—possesses its own integration resources and playbooks, which are adapted to regional operating environments and business characteristics. This decentralized approach reflects the company’s broader operating philosophy, which grants divisions meaningful autonomy while enforcing group-wide standards on financial reporting, operational benchmarks, and brand architecture.

The integration model follows a standardized but flexible framework. In the first phase, typically spanning the first 100 days post-close, Assa Abloy focuses on aligning financial systems, implementing its reporting structures, and establishing clear governance lines between the acquired business and the divisional management team. Operational integration—manufacturing consolidation, supply chain optimization, and sales force alignment—proceeds at a pace dictated by the specific characteristics of the acquired business. For small bolt-on acquisitions of regional lock manufacturers, operational integration can be swift and comprehensive, with the target’s production often migrating to existing Assa Abloy facilities within 12 to 24 months. For larger, more complex acquisitions—particularly in the technology segment—integration proceeds more cautiously, preserving the acquired company’s innovation culture and customer relationships while gradually embedding it into the Assa Abloy ecosystem.

Assa Abloy does not publicly disclose regular use of external integration advisors such as the major management consulting firms. The company’s integration maturity, built over three decades and hundreds of transactions, suggests that it has internalized the capabilities that less experienced acquirers must outsource. That said, it would be reasonable to assume that Assa Abloy engages external specialists for specific integration challenges—IT system migration, workforce restructuring in regulated labor markets, or complex carve-out situations—on a case-by-case basis. The company’s size and deal volume give it leverage to negotiate favorable terms with consulting firms, but the strategic direction of integration remains firmly in house.

One critical element of Assa Abloy’s integration approach deserves emphasis for practitioners studying the model: the company does not seek to homogenize acquired brands. Unlike some serial acquirers that rapidly rebrand acquisitions under a single corporate identity, Assa Abloy maintains a portfolio of local and regional brands that carry significant equity in their respective markets. Yale, for example, retains its distinct consumer identity in the residential segment, while HID Global operates with its own brand in the identity and credentialing space. This multi-brand strategy requires more sophisticated integration because the company must harmonize back-end operations and technology platforms while preserving distinct front-end market positions—a delicate balance that Assa Abloy has generally managed well.

Divestitures: Pruning the Portfolio with Purpose

Serial acquirers sometimes develop a reluctance to divest, treating every past acquisition as a permanent fixture in the portfolio. Assa Abloy has avoided this trap, demonstrating a willingness to divest businesses that no longer align with its strategic direction or that must be shed to satisfy regulatory requirements.

The most significant divestiture in Assa Abloy’s history involved the sale of certain businesses to secure regulatory approval for past acquisitions. During the HHI saga, Assa Abloy proposed divesting its Emtek and Smart Residential businesses (residential lock operations within its existing portfolio) to an independent buyer, Fortune Brands Innovations, in an attempt to resolve the DOJ’s competitive concerns. While the overall HHI deal ultimately collapsed, the proposed remedy divestiture illustrated Assa Abloy’s willingness to sacrifice existing assets to secure transformative acquisitions—a rational trade-off calculation, even though it failed to satisfy regulators in this instance.

Beyond regulatory-driven divestitures, Assa Abloy has periodically exited non-core product lines and geographies. These transactions tend to receive less public attention because they are typically smaller in scale—divesting a manufacturing plant in a non-strategic geography, selling a product line that falls outside the company’s evolving definition of “access solutions,” or exiting joint ventures that no longer fit. The strategic reasoning behind these divestitures is consistent: Assa Abloy concentrates capital and management attention on businesses where it can achieve or maintain a leadership position within the access solutions value chain. Product lines with commoditized margins, limited technology differentiation, or exposure to end markets outside the company’s core competence become divestiture candidates.

Assa Abloy does not publicly identify a preferred divestiture or carve-out advisory firm. Given the company’s primary orientation as an acquirer rather than a divester, its divestiture activity is episodic and does not require the type of standing advisory relationships that frequent divesting conglomerates might maintain. When divestitures arise, the company likely engages the same investment banks and law firms it works with on acquisitions, selecting based on the specific transaction’s requirements.

For M&A practitioners, Assa Abloy’s approach to divestitures offers a useful lesson in portfolio discipline. The company does not divest aggressively or frequently, but it treats divestiture as a legitimate strategic tool rather than an admission of failure. This balanced mindset—acquire with conviction, but prune without sentiment—contributes to the overall health of the acquisition program by ensuring that managerial bandwidth is allocated to the highest-returning businesses in the portfolio.

The Future: What Comes Next for Assa Abloy’s Acquisition Engine?

Predicting the precise targets of a serial acquirer is, naturally, an exercise in informed speculation. However, Assa Abloy’s strategic communications, industry trends, and historical patterns provide a credible basis for assessing the likely direction of future acquisitions.

First, the digital transformation of access control will continue to drive acquisition targeting. The global shift from mechanical keys to mobile credentials, biometric authentication, and cloud-managed access systems is still in its early stages across many geographies and end-market segments. Assa Abloy will almost certainly continue acquiring software-centric access control companies, cybersecurity firms with relevant authentication capabilities, and IoT platform providers that can integrate physical and digital access management. The company’s HID Global division serves as the natural home for many of these technology acquisitions, and its existing position in mobile access credentials (via its HID Mobile Access platform) provides a foundation on which to layer further capabilities through acquisition.

Second, entrance automation represents a growth vertical where Assa Abloy has room to expand. The global automatic door and pedestrian flow management market remains fragmented outside the top three players, and Assa Abloy has demonstrated that it views this segment as strategically important. Bolt-on acquisitions of regional entrance automation installers and service providers—particularly those with strong aftermarket service revenues—are likely targets.

Third, geographic expansion in emerging markets will sustain the pipeline of traditional bolt-on acquisitions. Sub-Saharan Africa, Southeast Asia, and parts of Latin America remain underpenetrated by institutional-grade access solutions. As these markets formalize and urbanize, demand for commercial and residential security hardware increases, creating acquisition opportunities among local manufacturers. Assa Abloy has followed this playbook in India and China over the past decade and will likely replicate it in frontier markets over the next five to ten years.

Fourth, the failed HHI acquisition may prompt Assa Abloy to recalibrate its approach to large-scale M&A in concentrated markets. The DOJ’s aggressive posture—and the broader global trend toward more interventionist antitrust enforcement—means that future mega-deals in the traditional lock and hardware space will face heightened regulatory risk. Assa Abloy may respond by focusing its larger acquisitions on adjacent segments (entrance automation, identity technology, software platforms) where its existing market share is lower and regulatory scrutiny is correspondingly less intense. Alternatively, the company may pursue “acquire and divest” strategies more proactively, packaging proposed divestitures into acquisition proposals from the outset to preempt regulatory objections.

Fifth, the growing emphasis on sustainability and energy efficiency in building design creates acquisition opportunities in smart building technology. Access control systems increasingly integrate with building management systems, HVAC controls, and energy monitoring platforms. Assa Abloy could selectively acquire companies at this intersection, extending its value proposition beyond the door and into the broader smart building ecosystem.

Under new CEO Nico Delvaux, who brings experience from Atlas Copco—another celebrated Swedish serial acquirer—the company’s acquisition discipline is likely to remain intact. Delvaux understands the Scandinavian model of decentralized management, continuous improvement, and acquisition-driven growth. His challenge will be to maintain the pace and quality of acquisitions while navigating a more complex regulatory environment and a portfolio that is increasingly weighted toward technology businesses requiring different integration skills than traditional manufacturing roll-ups.

Conclusion: Lessons from the World’s Largest Lock Company

Assa Abloy’s acquisition record offers M&A professionals several enduring lessons. Sustained deal velocity requires institutional processes, not heroic individual efforts. Strategic clarity must precede target identification, not follow it. Integration capability must be built as a permanent organizational muscle, not rented transaction by transaction. Portfolio discipline demands occasional divestitures, even from a company whose instinct is to acquire. And regulatory risk management has become a first-order strategic consideration for dominant acquirers, not merely a legal afterthought.

With over 300 acquisitions completed and a stated ambition to continue growing through M&A, Assa Abloy remains one of the most instructive case studies in the global serial acquirer landscape. The company has transformed an industry that many investors once dismissed as slow-growth and commoditized into a dynamic, technology-enabled platform generating double-digit returns on capital.

As antitrust regimes tighten globally and the shift from mechanical to digital access accelerates, Assa Abloy faces strategic choices that will define its next chapter. The company must balance its appetite for consolidation against regulatory constraints while simultaneously evolving its integration capabilities to absorb increasingly technology-oriented targets.

Given the rising regulatory barriers facing dominant acquirers worldwide, can serial acquirers like Assa Abloy sustain their historical deal pace, or will the next era of growth require a fundamentally different strategic playbook?

Leave a comment