Beyond the Balance Sheet: A 9-Point Checklist for Mastering Pension Liabilities in M&A

In the high-stakes world of mergers and acquisitions, dealmakers are trained to hunt for value and sniff out risk. We meticulously dissect financial statements, model synergies, and stress-test revenue projections. Yet, lurking deep within the target company’s structure is a liability that can be as financially potent as it is complex: the employee pension plan. Too often, these plans are treated as a simple line item on the balance sheet, a number to be plugged into a model. This is a perilous oversimplification. A poorly understood pension obligation can unravel a deal’s economics, trigger unforeseen cash contributions, and create a post-merger integration nightmare. It is the actuarial equivalent of discovering the beautiful vintage car you just acquired runs on a fuel that has not been produced since 1978.

Successfully integrating a target’s pension plan requires more than just financial acumen. It demands a sophisticated blend of actuarial science, legal expertise, operational foresight, and human resource strategy. The goal is not merely to absorb the liability but to manage it proactively, transforming a potential deal-breaker into a well-controlled component of the newly combined enterprise. This article provides a rigorous framework for M&A professionals to navigate this intricate landscape. We will first explore the foundational concepts and current trends shaping the world of pensions and then present a definitive nine-point checklist for assessing and integrating these complex obligations.

The Shifting Sands of Pension Liabilities: Core Concepts and Modern Trends

Before diving into a checklist, it is crucial to establish a common language and understand the environment in which these plans operate. Pension liabilities are not static; they are dynamic obligations influenced by market forces, changing demographics, and evolving regulations across the globe. A seasoned M&A team must appreciate these nuances to make informed decisions.

Words to Know: A Primer on Pension Plan Types

Not all pension plans are created equal, and the primary distinction dictates where the financial risk lies. Understanding this difference is the absolute first step in any analysis.

- Defined Contribution (DC) Plans: Think of a DC plan as an investment account. The company contributes a specified amount, such as a percentage of an employee’s salary, into an individual account. The employee often contributes as well and typically directs the investments within the account. The company’s obligation ends once its contribution is made. The ultimate retirement income depends on the contributions and the investment performance. For the acquirer, DC plans are wonderfully straightforward. The liability is predictable, transparent, and contained. Popular examples include 401(k) plans in the United States or similar personal account-based systems globally.

- Defined Benefit (DB) Plans: A DB plan is a promise. The company promises its employees a specific, predetermined retirement benefit, usually based on a formula involving salary history and years of service. The company is responsible for funding a trust to ensure it can meet these future promises, regardless of how the plan’s investments perform. Here, the company, and by extension the acquirer, bears all the investment and longevity risk. If the plan’s assets underperform or if retirees live longer than expected, the company must make up the shortfall. These are the plans that keep CFOs and M&A advisors awake at night.

- Multi-Employer Pension Plans (MEPPs): These are a special, and often more hazardous, category of DB plans. MEPPs involve multiple, typically unrelated, employers, often within the same industry and union. The risk is shared, but so is the liability, creating a “last-man-standing” scenario. If other participating companies go bankrupt or withdraw from the plan, the remaining employers can be held responsible for the unfunded obligations of the departed members’ employees. Acquiring a company that participates in an underfunded MEPP can expose the buyer to massive, unpredictable withdrawal liabilities that may dwarf the target’s own direct pension obligations.

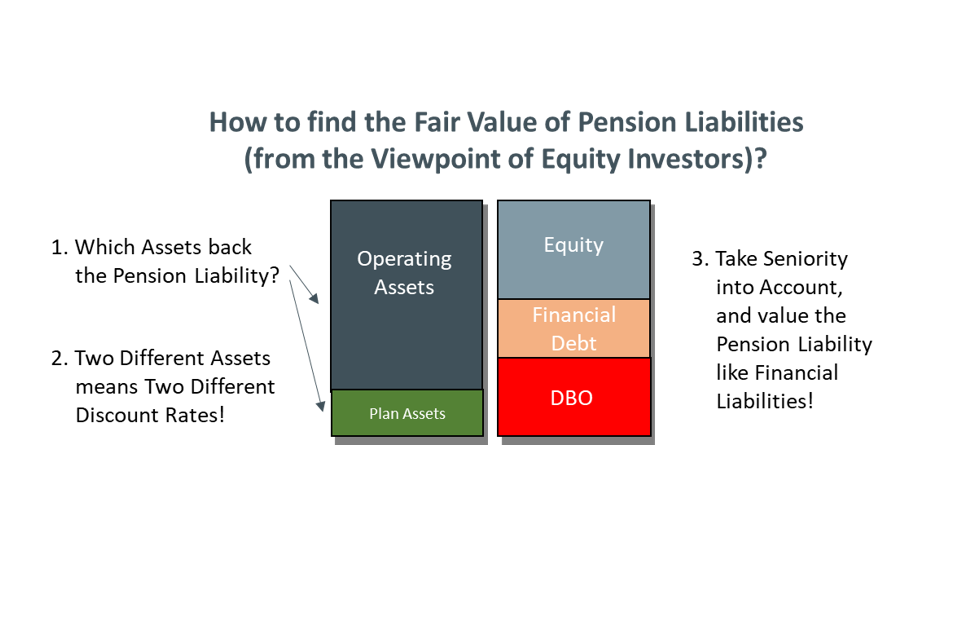

Valuing a defined benefit obligation goes beyond the single number on the balance sheet. This visual breaks down the investor’s perspective: the liability is backed by two different asset pools—the plan’s own investments and the company’s operating assets. This dual backing requires using different discount rates to accurately assess the true economic risk, treating the pension obligation with the same seriousness as financial debt.

Key Trends Shaping the Pension Landscape

The world of pensions is in constant flux. Several macro trends directly impact the risks and opportunities you will encounter during due diligence.

First, there is a decisive global shift away from DB plans toward DC plans. Companies have grown weary of the balance sheet volatility and open-ended risk associated with DB promises. This means that while you may acquire a target with a “frozen” DB plan (one that is closed to new entrants or no longer accruing new benefits), the legacy liability remains and must be managed for decades.

Second, fluctuating interest rates have a profound impact on DB plan funding. Pension liabilities are calculated by discounting future promised payments back to today’s value. When interest rates rise, the discount rate used also rises, which in turn lowers the present value of the liabilities, often improving a plan’s funded status. Conversely, falling rates inflate liabilities. An M&A team must analyze a plan’s sensitivity to interest rate changes to understand its true volatility. A plan that appears well-funded today could become significantly underfunded with a downward shift in rates.

Finally, regulatory oversight is tightening globally. Governments are increasingly focused on protecting employees’ retirement security, leading to stricter funding requirements, higher insurance premiums for DB plans (like those paid to the Pension Benefit Guaranty Corporation in the US), and more complex reporting mandates. This regulatory web adds another layer of legal and compliance risk that must be navigated, with different rules applying in every jurisdiction.

The Definitive 9-Point Checklist for Pension Integration

With this foundational understanding, we can now move to a practical, actionable framework. Following this checklist will ensure a comprehensive and disciplined approach to evaluating and integrating a target’s employee pension plans.

1. Mobilize Expert Diligence Early

Pension analysis is not a task for generalists. Long before the letter of intent is finalized, you must engage a specialized team. This team should include an ERISA (or country-specific pension law) attorney, an enrolled actuary, and an HR benefits consultant. Attempting to save costs by delaying their involvement is a classic mistake. These experts can quickly identify red flags in the initial data room that could fundamentally alter the valuation and structure of the deal. Are there signs of a distressed MEPP? Is the DB plan subject to unusual government restrictions? Early expert review allows you to ask the right questions and demand the right data from the seller from the very beginning.

2. Classify and Catalog Every Plan, Everywhere

The first task for your diligence team is to create a comprehensive inventory of every single retirement plan the target sponsors, participates in, or has ever contributed to, across all geographic locations. This is not just about the primary corporate plan. You must uncover plans within subsidiaries, foreign operations, and joint ventures. Each plan must be classified: Is it a DB, DC, or hybrid plan? Is it a single-employer plan or a MEPP? Is it active, frozen, or terminated but still distributing assets? This detailed catalog forms the map for your entire analysis. Overlooking a small, forgotten plan in a foreign subsidiary can lead to unexpected post-closing surprises.

3. Quantify the True Financial Obligation

This step goes far beyond accepting the pension liability figure presented on the target’s balance sheet. Accounting standards (like ASC 715 in the US or IAS 19 internationally) provide a snapshot, but they do not tell the whole story. Your actuary must perform an independent valuation of the DB plans. This involves scrutinizing the seller’s assumptions—like the discount rate, expected return on assets, salary growth projections, and mortality tables—and stress-testing them against more conservative, market-based assumptions. This analysis should yield three critical numbers: the accounting liability, the funding liability required by regulators, and the “plan termination” liability, which represents the full cost to settle all obligations today. The gap between these figures reveals the true economic risk.

4. Scrutinize Legal and Regulatory Compliance

Your legal expert’s mission is to hunt for non-compliance, hidden triggers, and contractual time bombs. They must review all plan documents, trust agreements, summary plan descriptions, and government filings. Have all required contributions been made on time? Has the plan passed all non-discrimination testing? Are there any pending audits or litigation with regulators or plan participants? Crucially, the attorney must check for “change of control” provisions within plan documents or union agreements. These clauses can trigger accelerated funding requirements, benefit enhancements, or other costly events upon the closing of an acquisition.

5. Assess Administrative and Operational Synergies (or Headaches)

A pension plan is not just a financial entity; it is an operating one. Your diligence should investigate the “how” of the plan’s management. Who are the current administrators, trustees, and investment managers? What are their fees and performance records? What technology platforms are used for recordkeeping and employee communication? Understanding the administrative infrastructure is key to planning for integration. If your company uses a single global recordkeeper and the target uses a dozen different vendors, the path to consolidation will be complex and costly. Identifying these operational disconnects early allows you to accurately budget for integration expenses.

6. Model Future Scenarios and Define Your Integration Strategy

Once you have a firm grasp of the financials, legal standing, and operations, you can begin to strategize. You do not have to simply inherit the target’s plan as-is. Several strategic options exist, and your team should model the financial and human impact of each:

- Freeze the Plan: Close the DB plan to new hires and/or stop existing participants from accruing further benefits. This caps the growth of the liability but leaves the legacy obligation to be managed.

- Merge the Plan: Combine the target’s plan with your own existing plan. This can create administrative efficiencies but requires a complicated “merger of equals” analysis to ensure no participant’s accrued benefits are reduced. This is often only feasible if the plans are of a similar type and in the same jurisdiction.

- Terminate the Plan: This is the most decisive but often most expensive option. It involves paying out all accrued benefits, either through lump-sum payments to participants or by purchasing a group annuity contract from an insurance company to take over the payment obligations. This removes the liability from your balance sheet entirely but often requires a significant, immediate cash outlay to fully fund the plan on a termination basis.

7. Structure the Deal to Mitigate Risk

The findings from your diligence must be directly translated into the sale and purchase agreement (SPA). If the DB plan is significantly underfunded, you should negotiate a purchase price reduction to reflect the economic reality of the liability you are inheriting. Alternatively, you can use other structural protections. You might require the seller to make a pre-closing contribution to the plan to bring it to a certain funding level. For risks that are uncertain or hard to quantify, such as a potential MEPP withdrawal liability, you can negotiate for a specific indemnity from the seller or place a portion of the purchase price into escrow for a set period.

8. Develop a Meticulous Communication Masterplan

Integrating pension plans directly affects employees’ financial security and peace of mind. A failure to communicate clearly, transparently, and empathetically can breed anxiety, erode trust, and damage morale in the newly combined company. You must develop a detailed communication plan well before the deal closes. This plan should outline what will be said, by whom, to which employee groups, and when. All communications must be legally vetted to avoid making inadvertent promises or misstating complex plan changes. The goal is to provide certainty and reassurance during a period of intense uncertainty.

9. Execute a Disciplined Post-Merger Integration (PMI)

The deal is signed, and the integration begins. This is where strategy meets execution. A dedicated PMI team, including representatives from HR, finance, legal, and IT, must be tasked with implementing the chosen pension strategy. This involves a host of detailed actions: filing the necessary documents with regulators, coordinating with plan administrators and trustees to transfer assets or merge systems, mapping employee data, and rolling out the employee communication plan. This process can take months, or even years, and requires rigorous project management to ensure every “i” is dotted and every “t” is crossed. Overlooking a single administrative step can lead to compliance failures and employee complaints down the line.

From Liability to Strategic Advantage

Assumed pension liabilities represent one of the most technically challenging aspects of M&A integration. They are a potent mix of financial risk, legal complexity, and human sensitivity. Approaching them as a mere accounting entry is an invitation for post-deal regret. However, by adopting a structured, multi-disciplinary approach, a savvy acquirer can demystify the risk, quantify the true cost, and execute a seamless integration. A well-managed pension strategy does more than just protect the deal’s value; it demonstrates a commitment to employee welfare and lays the groundwork for a stable and successful combined organization. By turning a spotlight on this often-shadowed corner of due diligence, you can transform a potential liability into a testament to your firm’s strategic discipline.

What has been the most unexpected pension-related challenge you have encountered in a deal, and how did your team navigate it?

Leave a comment