Locking In the Deal: Why Proactive FX Hedging Is a Non-Negotiable for Cross-Border M&A With Extended Closing Periods

Cross-border mergers and acquisitions operate at the intersection of strategic ambition and operational complexity. Dealmakers must navigate regulatory approvals across multiple jurisdictions, reconcile divergent accounting standards, satisfy antitrust authorities on different continents, and align stakeholders who may not share a common language — let alone a common currency. Among these challenges, one risk factor remains stubbornly underappreciated until the moment it inflicts real damage: foreign exchange exposure during extended closing periods.

Between signing and closing, months can pass. In complex cross-border transactions involving regulatory review in the European Union, China, or multiple emerging markets, that gap can stretch to nine, twelve, or even eighteen months. During that window, the acquirer has committed to a purchase price denominated in a foreign currency, but the actual cash outflow has not yet occurred. The deal value, in the acquirer’s home currency terms, floats on the open sea of exchange rate volatility. A five percent currency swing on a ten-billion-dollar deal translates to a five-hundred-million-dollar change in effective cost — a figure large enough to erase the projected synergies that justified the transaction in the first place.

Proactive foreign exchange hedging exists to close this gap between commitment and completion. It transforms a known risk into a managed cost, and it does so best when implemented early, structured deliberately, and monitored continuously. Yet many experienced dealmakers still treat FX hedging as a treasury afterthought rather than a core component of deal strategy. This article examines why that approach is insufficient, explains how proactive hedging strategies work in cross-border M&A, and draws on real-world examples to illustrate the tangible value of getting this right.

Understanding the Core Concepts

What Is Foreign Exchange Hedging?

Foreign exchange hedging is the practice of using financial instruments to reduce or eliminate the risk that adverse currency movements will negatively affect the value of an anticipated transaction, asset, or cash flow denominated in a foreign currency. At its most basic level, hedging means locking in a known exchange rate for a future date, so that the party bearing the exposure can plan, budget, and execute with financial certainty.

The most common instruments used in FX hedging include forward contracts, currency options, and cross-currency swaps. A forward contract obligates two parties to exchange a specified amount of one currency for another at a predetermined rate on a future date. A currency option gives the holder the right, but not the obligation, to exchange currencies at a set rate, providing protection against downside moves while preserving the ability to benefit from favorable shifts. Cross-currency swaps involve exchanging principal and interest payments in different currencies over time and are more commonly used for ongoing operational hedging or financing structures than for single-transaction deal hedging.

Each instrument carries different cost profiles, levels of flexibility, and accounting implications. The choice among them depends on the degree of certainty about deal completion, the magnitude and direction of the perceived currency risk, the acquirer’s risk appetite, and the accounting treatment the company seeks.

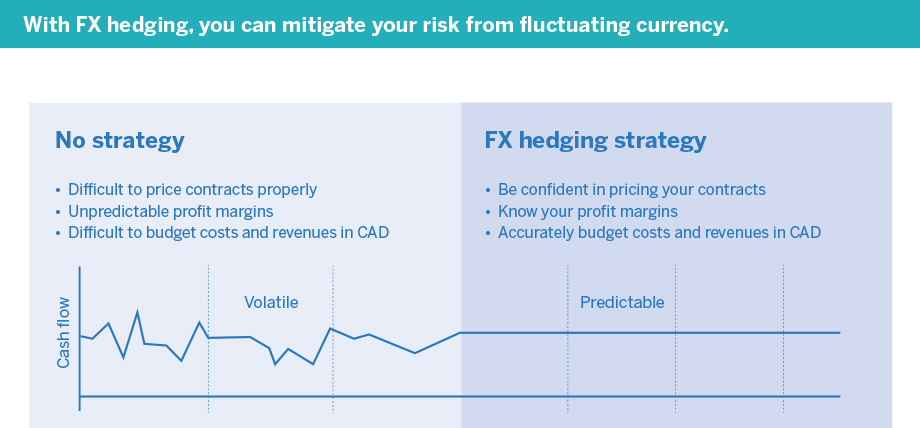

Side-by-side comparison showing how an unhedged approach produces volatile, unpredictable currency exposure — making it difficult to price contracts and budget accurately — while a proactive FX hedging strategy delivers a predictable, stable cost line that protects profit margins and supports confident financial planning in cross-border transactions.

What Makes FX Hedging “Proactive”?

The distinction between reactive and proactive hedging is not merely semantic — it is strategic. Reactive hedging occurs when a company scrambles to put protection in place after a currency move has already begun to erode deal economics. Proactive hedging, by contrast, integrates FX risk management into the deal process from the earliest stages of transaction planning, typically well before signing or immediately upon execution of the definitive agreement.

A proactive approach involves several critical steps: quantifying the FX exposure as part of initial deal modeling, stress-testing the transaction’s returns under multiple currency scenarios, selecting hedging instruments and structures during the due diligence phase, establishing trigger points and decision frameworks for implementation, and building ongoing monitoring protocols that adapt the hedge as deal timing and probability evolve.

Proactive hedging recognizes that FX risk is not a peripheral nuisance but a first-order variable that can fundamentally alter the strategic and financial rationale of a cross-border deal. Treating it as such, from the beginning, is what separates disciplined acquirers from those who discover the cost of inaction on closing day.

Current Trends Amplifying the Need

Several macro trends have intensified the relevance of proactive FX hedging for cross-border dealmakers. Global currency volatility has remained elevated since the pandemic-era disruptions, driven by divergent monetary policy cycles across the Federal Reserve, European Central Bank, Bank of Japan, and emerging market central banks. Geopolitical fragmentation — including trade tensions, sanctions regimes, and supply chain realignment — has introduced sudden, sharp currency moves that historical models struggle to predict.

Simultaneously, deal closing timelines have lengthened. Regulatory scrutiny of cross-border transactions has intensified, particularly from competition authorities in the EU, the UK’s Competition and Markets Authority, China’s State Administration for Market Regulation, and the expanded scope of foreign investment screening regimes worldwide. The Committee on Foreign Investment in the United States (CFIUS) and its equivalents in other jurisdictions add further layers of review. The result is that the average time between signing and closing for large cross-border deals has trended upward over the past decade, giving currency markets more time to move — and more room to inflict damage.

Against this backdrop, the question for cross-border acquirers is not whether FX risk matters, but how seriously they are willing to manage it.

Three Pillars of Value: Why Proactive FX Hedging Matters

1. Preserving Deal Economics and Protecting Returns

The most direct and quantifiable value of proactive FX hedging lies in preserving the financial assumptions that underpin the transaction. When an acquirer’s board approves a cross-border deal, it does so based on a financial model that incorporates a specific purchase price, projected synergies, a cost of capital, and an expected return. That model is built using exchange rate assumptions that reflect conditions at or near the time of signing.

If the acquirer’s home currency weakens materially against the target’s currency during an extended closing period, the effective purchase price rises in home-currency terms. The synergies do not change, but the price paid to achieve them does — and internal rate of return compresses accordingly. In severe cases, the return can fall below the hurdle rate that justified the acquisition, turning a value-creating deal into a value-destroying one without any change in the target’s business performance.

Proactive hedging addresses this by locking in the exchange rate embedded in the approved deal model. A forward contract executed at signing, sized to match the expected purchase price and timed to the anticipated closing date, ensures that the acquirer pays an effective price consistent with the economics it underwrote. If the hedge is executed early, before market conditions shift, the forward rate is typically close to the spot rate adjusted for the interest rate differential between the two currencies — a well-understood and generally modest cost.

This preservation function matters most for deals with thin synergy margins or high leverage, where even modest currency moves can meaningfully affect debt service coverage ratios, post-closing leverage, and the acquirer’s ability to achieve its integration plan within the projected financial framework.

2. Reducing Uncertainty and Strengthening Stakeholder Confidence

Cross-border M&A transactions involve a wide constellation of stakeholders, each of whom bears some form of exposure to the deal’s financial outcomes. Shareholders evaluate whether the acquisition will be accretive. Lenders underwrite financing commitments based on projected cash flows and leverage ratios. Board members approve the transaction based on financial projections and risk assessments. Regulators and rating agencies scrutinize the acquirer’s post-deal financial stability.

Unhedged FX exposure introduces a variable that none of these stakeholders can control and that all of them find uncomfortable. When an acquirer announces a major cross-border transaction without disclosing a coherent FX risk management strategy, sophisticated investors and analysts notice.

Rating agencies may flag the exposure as a risk factor in their assessment of the acquirer’s creditworthiness. Lenders may build wider pricing buffers into acquisition financing to compensate for the currency uncertainty, or they may impose conditions requiring hedging as a covenant.

By contrast, an acquirer that presents a clear, proactive hedging strategy alongside the deal announcement sends a signal of financial discipline and risk awareness. It reassures the market that the deal’s projected returns are protected against a foreseeable and manageable risk. It gives lenders confidence in the stability of debt service projections. It allows the board to evaluate the transaction on its strategic merits rather than worrying about whether a currency shock will undermine the financial case between approval and completion.

This confidence-building function extends internally as well. Integration planning teams working on post-close value creation benefit from knowing that the financial starting point of the combined entity will be consistent with the plan, rather than subject to a currency-driven surprise that could force immediate budget revisions or strategic recalibrations.

3. Enabling Strategic Flexibility During the Closing Period

The third, and perhaps most underappreciated, value of proactive FX hedging is the strategic flexibility it provides the acquirer during the often-turbulent period between signing and closing. Extended closing periods are not passive waiting rooms. They are active phases during which regulatory negotiations evolve, market conditions shift, competing bids may emerge, and the acquirer must make ongoing decisions about financing structure, integration planning, and communication strategy.

An unhedged FX exposure acts as an anchor on this flexibility. If the acquirer’s home currency weakens significantly, management may face pressure to renegotiate deal terms, seek additional financing, or reconsider the transaction altogether — not because the strategic rationale has changed, but because the currency-driven cost increase has altered the financial calculus. These discussions are distracting, time-consuming, and can introduce friction with the target’s management or shareholders at a moment when trust and collaboration are essential.

A well-structured hedging program removes this distraction. Management can focus on securing regulatory approvals, planning integration, and managing stakeholder communications without the background noise of an escalating currency exposure. If the deal timeline extends beyond original expectations — a common occurrence in complex cross-border transactions — the hedge can often be rolled or restructured to match the new closing date, provided the hedging strategy was designed with this contingency in mind.

Furthermore, proactive hedging supports optionality in deal structuring. If the acquirer has locked in its FX rate, it can evaluate alternative financing structures, consider adjusting the mix of cash and stock consideration, or respond to changes in interest rate markets without simultaneously managing a moving currency target. In negotiations with regulators who may require divestitures or remedies that affect deal value, the acquirer benefits from knowing that at least one major financial variable — the exchange rate — is under control.

Real-World Cases: Proactive FX Hedging in Practice

Case 1: Bayer’s Acquisition of Monsanto — Protecting a Mega-Deal Across a Two-Year Closing Window

Bayer’s acquisition of Monsanto, announced in September 2016 and closed in June 2018, stands as one of the most prominent examples of a cross-border mega-deal with an extended closing period. The all-cash transaction valued Monsanto at approximately $63 billion, payable in U.S. dollars by a euro-denominated acquirer. The closing period stretched to nearly twenty-one months, driven by extensive antitrust reviews across more than thirty jurisdictions.

During that window, the EUR/USD exchange rate experienced meaningful fluctuations, moving from approximately 1.12 at announcement to a range that at times exceeded 1.24 — a swing that, left unhedged, would have increased the euro cost of the acquisition by billions. Bayer employed a comprehensive FX hedging program using forward contracts and options to manage this exposure, aligning the currency protection with the anticipated closing timeline and adjusting as regulatory review extended the deal’s completion date.

This case illustrates the first pillar of value — preserving deal economics. By hedging proactively, Bayer ensured that the effective euro cost of the acquisition remained within the parameters approved by its board and communicated to its shareholders, even as the underlying exchange rate moved substantially over a closing period that few could have predicted would last nearly two years.

Case 2: SoftBank’s Acquisition of ARM Holdings — Stakeholder Confidence Through Currency Discipline

When SoftBank announced its acquisition of UK-based ARM Holdings in July 2016 for approximately £24.3 billion, the deal landed in the immediate aftermath of the Brexit referendum, a period of extreme volatility for the British pound. The GBP had fallen sharply against the Japanese yen and the U.S. dollar, and uncertainty about the UK’s economic trajectory was at a peak.

SoftBank, a Japanese acquirer paying in sterling, faced a complex FX environment. The weakened pound actually reduced the yen cost of the acquisition relative to pre-Brexit levels, but the risk of further volatility — in either direction — was substantial. SoftBank moved quickly to secure financing and lock in currency exposure, utilizing a combination of bridge loans denominated in multiple currencies, committed FX hedges, and a structured financing approach that reduced the sensitivity of the total acquisition cost to further GBP/JPY movements.

The deal closed in September 2016, just over two months after announcement — a relatively short window. However, SoftBank’s disciplined approach to managing the currency dimension of the transaction reassured investors and lenders during a period of acute market anxiety. This case demonstrates the second pillar of value: reducing uncertainty and strengthening stakeholder confidence. By addressing FX risk head-on and immediately, SoftBank reinforced the credibility of its financial plan at a time when markets were questioning the stability of the very currency in which the deal was denominated.

Case 3: Linde and Praxair Merger — Strategic Flexibility Across Regulatory Complexity

The merger of equals between Linde AG and Praxair, announced in June 2017 and closed in October 2018, created the world’s largest industrial gas company in a transaction valued at approximately $90 billion. The deal involved a German-listed entity and a U.S.-listed entity, required regulatory clearance in over thirty jurisdictions, and demanded significant divestitures to satisfy competition authorities in multiple markets.

The sixteen-month closing period exposed both parties to sustained EUR/USD volatility. Given the merger-of-equals structure, the currency dynamics were especially complex — exchange rate movements affected the relative value of the consideration, the combined entity’s projected financials, and the terms of the required divestitures. Both companies employed hedging strategies to manage their respective currency exposures, and the transaction’s financial advisors structured the deal terms with explicit attention to FX sensitivity.

Crucially, the proactive management of currency risk allowed Linde and Praxair to focus their negotiating energy on the complex regulatory remedies required to secure approval — including the divestiture of significant business segments in multiple countries — without being simultaneously destabilized by currency-driven shifts in deal value. This case exemplifies the third pillar of value: enabling strategic flexibility. The hedging programs gave both management teams the bandwidth to navigate a demanding regulatory process, restructure the deal where necessary, and ultimately close a transformative transaction on financial terms that remained consistent with the original strategic vision.

Key Considerations for Execution

Proactive FX hedging is not a set-and-forget exercise. Effective execution requires attention to several critical factors throughout the deal lifecycle.

Hedge sizing and timing must reflect a realistic assessment of deal certainty. Hedging the full notional amount of the purchase price on day one assumes a one-hundred-percent probability of closing, which is rarely the case. A staged approach — hedging a portion of the exposure at signing and increasing hedge coverage as regulatory milestones are cleared — balances protection against the cost of unwinding hedges if the deal fails.

Instrument selection should align with the company’s accounting objectives and risk tolerance. Forward contracts offer simplicity and certainty but create a loss if the deal does not close and the currency has moved favorably. Options cost an upfront premium but provide asymmetric protection: they cap downside exposure while preserving upside participation, and they do not create an obligation if the deal terminates.

Tenor management is essential when closing timelines are uncertain. Hedges structured to a specific closing date may need to be rolled if regulatory review extends the timeline. Building flexibility into the hedge structure — through rolling forwards, options with extendable exercise dates, or layered hedging across multiple potential closing dates — prevents the acquirer from being caught with expiring hedges and reopened exposure.

Accounting treatment under IFRS and U.S. GAAP requires careful navigation. Hedge accounting, when achievable, allows the gains and losses on hedging instruments to be matched against the underlying transaction in the financial statements, avoiding earnings volatility. Qualifying for hedge accounting demands formal documentation, effectiveness testing, and ongoing compliance, all of which should be planned at the outset.

Counterparty risk deserves consideration, particularly for large-notional hedges with extended tenors. Using multiple bank counterparties and monitoring credit exposure throughout the closing period reduces concentration risk.

Finally, communication matters. The hedging strategy should be documented in board materials, disclosed appropriately in transaction filings, and explained to key stakeholders — including lenders, rating agencies, and equity analysts — so that its protective role is understood and valued.

Conclusion

Cross-border M&A with extended closing periods exposes acquirers to a financial risk that is entirely foreseeable and substantially manageable, yet too often inadequately addressed. Proactive foreign exchange hedging preserves the deal economics that justified the transaction, strengthens confidence among the stakeholders whose support the deal requires, and frees management to focus on the strategic and regulatory challenges that ultimately determine whether the transaction succeeds.

The tools are well understood. Forward contracts, options, and structured hedging programs have been used effectively across decades of cross-border deal activity. The analytical frameworks for sizing, timing, and structuring hedges are robust and widely available. The cost of hedging, while real, is modest relative to the magnitude of the exposure it manages — and trivial compared to the potential cost of leaving the exposure open.

What remains is a question of discipline and organizational culture. Companies that embed FX risk management into their M&A process from the earliest stages of deal origination consistently achieve better financial outcomes than those that defer the question to treasury after the deal is signed. In a world of persistent currency volatility, lengthening regulatory timelines, and increasingly complex cross-border transactions, proactive hedging is not a luxury — it is a fundamental component of sound dealmaking.

As you evaluate your next cross-border acquisition, consider this: if your deal model cannot survive a ten percent adverse currency move between signing and closing, can you really afford not to hedge from day one?

Leave a comment