When Revenue Isn’t What It Seems: 7 Ways ASC 606 and IFRS 15 Can Transform Your M&A Target’s Valuation

In the world of mergers and acquisitions, revenue has long served as the north star of valuation. Buyers project future cash flows, apply multiples to earnings, and build elaborate models—all anchored to a single, seemingly straightforward number: the top line. Yet since 2018, that number has become considerably less straightforward. The introduction of ASC 606 in the United States and IFRS 15 internationally fundamentally rewrote the rules governing when and how companies recognize revenue. For M&A practitioners who cut their teeth under the old standards, the implications run far deeper than a mere accounting exercise.

These standards do not simply shuffle numbers between reporting periods. They redefine contractual boundaries, reallocate transaction prices across performance obligations, and introduce judgment-laden estimates where once there were bright-line rules. The result is a valuation landscape where two identical businesses with identical economic substance can report materially different revenue figures depending on how they interpret the new guidance. For acquirers, this creates both risk and opportunity. For sellers, it demands a new level of financial storytelling sophistication.

This article examines how ASC 606 and IFRS 15 reshape M&A due diligence and valuation. It begins with the foundational concepts necessary to understand these standards, explores the broader trends affecting deal professionals, and then presents seven specific ways revenue recognition changes can materially affect a target company’s valuation. Whether you are acquiring a software company with complex licensing arrangements or a construction firm with long-term contracts, understanding these dynamics has become essential to avoiding costly surprises at the closing table.

The Foundation: Understanding ASC 606 and IFRS 15

What These Standards Actually Do

ASC 606, formally titled “Revenue from Contracts with Customers,” represents the Financial Accounting Standards Board’s comprehensive overhaul of U.S. GAAP revenue recognition guidance. IFRS 15, issued by the International Accounting Standards Board, is its virtually identical international counterpart. Both standards emerged from a joint convergence project that took over a decade to complete, and both became effective for most public companies in 2018.

Before these standards arrived, revenue recognition operated under a patchwork of industry-specific rules. Software companies followed one set of guidance, construction companies another, and service providers yet another. This fragmentation created inconsistency, reduced comparability across industries, and occasionally invited aggressive accounting practices that recognized revenue earlier than economic reality justified.

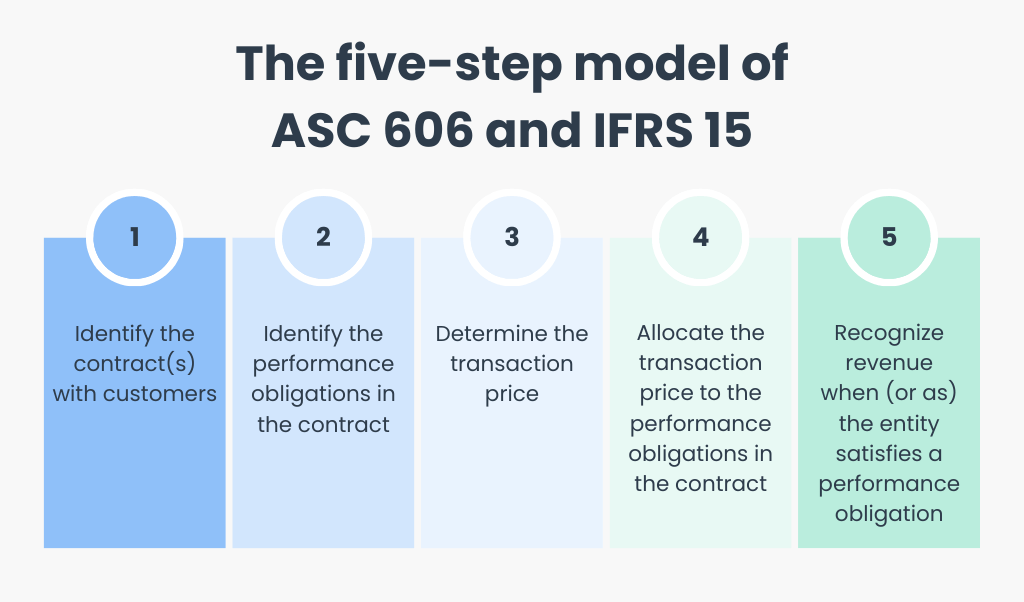

ASC 606 and IFRS 15 replaced this fragmented landscape with a single, principles-based framework organized around five steps: identify the contract with the customer, identify the performance obligations in the contract, determine the transaction price, allocate the transaction price to the performance obligations, and recognize revenue when (or as) each performance obligation is satisfied. This five-step model applies universally, whether the company sells jet engines, software licenses, or consulting services.

An infographic illustrating the five-step revenue recognition model under ASC 606 and IFRS 15, outlining the sequential steps: (1) identify the contract(s) with customers, (2) identify performance obligations, (3) determine the transaction price, (4) allocate the transaction price to performance obligations, and (5) recognize revenue when performance obligations are satisfied.

Why Convergence Mattered

The convergence of U.S. and international standards addressed a genuine problem in global capital markets. Before ASC 606 and IFRS 15, a multinational corporation might report different revenue figures to different investor bases depending on which accounting framework applied. Cross-border M&A transactions required extensive reconciliation work to understand what a target’s revenue would look like under the acquirer’s reporting framework. The new standards largely eliminated this friction for revenue recognition, creating a common language for the first time.

For M&A professionals, this convergence offers clear benefits. A U.S.-based acquirer evaluating a European target now works with revenue recognition principles that are substantively identical. The same analytical frameworks apply regardless of geographic origin. However, this convergence also means that the complexities embedded in ASC 606 and IFRS 15 now affect virtually every cross-border transaction, making mastery of these standards a baseline requirement for sophisticated deal work.

Key Concepts Every Deal Professional Must Know

Several concepts within ASC 606 and IFRS 15 carry particular significance for M&A valuation. Understanding these terms is essential before examining their deal implications.

Performance obligations represent the unit of account for revenue recognition. A single contract may contain multiple performance obligations—distinct promises to transfer goods or services to the customer. Identifying these obligations requires judgment, and different conclusions can dramatically affect the timing and amount of revenue recognition.

The transaction price encompasses the amount of consideration a company expects to receive in exchange for transferring goods or services. This calculation becomes complex when contracts include variable consideration such as bonuses, penalties, rebates, or rights of return. Companies must estimate these variable amounts and include them in the transaction price only to the extent that a significant reversal is not probable.

Standalone selling price determines how the transaction price gets allocated across multiple performance obligations. When a company bundles products and services together, it must allocate the total contract price based on the relative standalone selling prices of each component. These allocations directly affect when revenue hits the income statement.

Over time versus point in time recognition distinguishes between performance obligations satisfied continuously and those satisfied at a discrete moment. Construction contracts, long-term service arrangements, and certain customized manufacturing engagements typically qualify for over-time recognition. Product sales and standard software licenses generally recognize revenue at a point in time. The distinction profoundly affects revenue patterns and working capital dynamics.

Current Trends Reshaping the Landscape

Increased Scrutiny from Regulators and Auditors

Since ASC 606 became effective, the Securities and Exchange Commission has issued numerous comment letters challenging companies’ revenue recognition policies. The Public Company Accounting Oversight Board has similarly flagged revenue recognition as a persistent audit deficiency area. This heightened regulatory attention translates directly to M&A due diligence. Acquirers can no longer assume that audited financial statements reflect appropriate application of ASC 606. Indeed, the judgment-intensive nature of these standards means that reasonable professionals can reach different conclusions about the same contract.

Quality of Earnings Adjustments Proliferate

Quality of earnings reports prepared in M&A transactions increasingly focus on ASC 606 compliance issues. Advisors now routinely examine whether targets have appropriately identified performance obligations, correctly estimated variable consideration, and applied defensible standalone selling price allocations. These analyses frequently produce adjustments that change EBITDA by meaningful amounts, directly affecting purchase price negotiations. The days when revenue recognition received cursory attention in due diligence have definitively ended.

Software and Technology Transactions Lead the Complexity

Technology transactions face particularly acute ASC 606 challenges. Software-as-a-service arrangements, hybrid on-premise and cloud deployments, platform businesses with multiple revenue streams, and contracts bundling software with implementation services all present complex judgment calls under the new standards. The venture capital and private equity communities have invested heavily in understanding these issues, recognizing that growth-stage technology companies often lack the accounting infrastructure to implement ASC 606 optimally.

Private Company Considerations

While public companies implemented ASC 606 years ago, many private companies continue to operate under the old standards or have implemented ASC 606 inconsistently. When a public acquirer purchases a private target, the post-acquisition accounting conversion can reveal material differences between the revenue figures used in deal negotiations and the revenue figures that will appear in the acquirer’s consolidated financial statements. Sophisticated buyers now address this risk explicitly in purchase agreements.

Seven Ways Revenue Recognition Changes Can Affect a Target’s Valuation

The principles embedded in ASC 606 and IFRS 15 interact with M&A valuation in specific, identifiable ways. Each of the following seven areas represents a potential source of value creation, value destruction, or negotiating leverage depending on where you sit at the deal table.

1. Contract Bundling Reallocates Value Across Deliverables

When targets bundle multiple products or services into a single contract, ASC 606 requires allocation of the total transaction price based on relative standalone selling prices. This allocation can shift revenue between periods and between deliverables in ways that affect valuation metrics.

Consider a software company that sells a perpetual license bundled with three years of maintenance. Under the old standards, this company might have allocated 80% of the contract value to the upfront license and 20% to maintenance, recognizing most revenue immediately. Under ASC 606, if the standalone selling prices suggest a 50/50 split, revenue recognition shifts materially toward the maintenance period. The same economic arrangement produces a different revenue trajectory, a different EBITDA profile, and potentially a different valuation multiple.

Acquirers should examine how targets establish standalone selling prices and whether those determinations reflect genuine market evidence. Inflated standalone selling prices for upfront deliverables can accelerate revenue recognition in ways that do not survive post-acquisition scrutiny.

2. Variable Consideration Introduces Estimation Risk

Many commercial arrangements include variable consideration elements: performance bonuses, volume rebates, early payment discounts, penalties for late delivery, or rights of return. ASC 606 requires companies to estimate these variable amounts and include them in the transaction price, subject to a constraint designed to prevent significant revenue reversals.

The estimation methods targets employ—and the assumptions underlying those estimates—directly affect reported revenue. A target that aggressively estimates variable consideration will report higher revenue than an economically identical target using conservative assumptions. During due diligence, acquirers should examine historical accuracy of variable consideration estimates. If actual outcomes consistently fall below estimates, the target’s revenue may be systematically overstated.

This issue becomes particularly acute in industries with significant return rights or rebate arrangements. Consumer products companies, pharmaceutical distributors, and certain retail businesses all face substantial variable consideration estimation challenges that merit careful due diligence attention.

3. Contract Modifications Can Reset the Accounting

When parties modify existing contracts, ASC 606 prescribes specific accounting treatments depending on whether the modification adds distinct goods or services and whether pricing reflects standalone selling prices. Some modifications are accounted for as separate contracts, some require prospective treatment, and some require cumulative catch-up adjustments.

Targets with frequent contract modifications—common in long-term service arrangements, construction, and enterprise software—may face significant accounting complexity. The treatment of a single modification can affect revenue recognition for the entire contract relationship. Acquirers should understand how targets account for modifications and whether those treatments are consistent, defensible, and appropriately documented.

Contract modification accounting also creates due diligence opportunities. If a target has accounted for modifications inconsistently, post-acquisition corrections may shift revenue between periods in ways that affect earnout calculations, purchase price adjustments, or representations and warranties exposure.

4. Principal Versus Agent Determinations Affect Gross Revenue

ASC 606 requires companies to determine whether they act as principal or agent in arrangements where another party is involved in providing goods or services to the customer. Principals recognize revenue at the gross amount collected from customers. Agents recognize revenue only for the fee or commission they retain.

This determination hinges on whether the company controls the specified good or service before it transfers to the customer. Control represents a facts-and-circumstances judgment that reasonable professionals may assess differently. A target that concludes it acts as principal will report higher revenue—though not higher gross profit—than an identical target that concludes it acts as agent.

For acquirers using revenue multiples to value targets, the principal versus agent determination directly affects valuation. A company reporting $100 million in gross revenue valued at 3x revenue has a $300 million implied enterprise value. The same company reporting $20 million in net revenue as an agent, valued at the same 3x multiple, has a $60 million implied enterprise value. Understanding the substance of the target’s role in commercial arrangements is essential to applying appropriate valuation methodologies.

5. Timing of Revenue Recognition Shifts Working Capital Dynamics

The transition from industry-specific guidance to ASC 606 shifted revenue recognition timing for many companies. Some recognized revenue earlier under the new standard; others recognized it later. These timing differences affect not only reported profitability but also working capital patterns.

A company that now recognizes revenue earlier than it previously did will show higher contract assets (unbilled receivables) and potentially lower deferred revenue. Conversely, a company that recognizes revenue later will accumulate larger deferred revenue balances. These balance sheet changes directly affect net working capital calculations in purchase agreements.

Acquirers should understand how ASC 606 adoption affected the target’s working capital patterns. Working capital targets and adjustment mechanisms in purchase agreements should reflect the company’s current accounting policies, not historical patterns that may no longer apply. Failure to align these provisions with ASC 606 realities can create post-closing disputes over purchase price adjustments.

6. Deferred Revenue May Not Equal Future Performance

Under the old standards, deferred revenue generally represented cash collected for services not yet rendered. The balance provided a reasonable proxy for contracted future performance obligations. Under ASC 606, the relationship between deferred revenue and remaining performance obligations has become more complex.

ASC 606 introduced required disclosures about remaining performance obligations—the aggregate transaction price allocated to unsatisfied or partially satisfied performance obligations. This figure can differ significantly from deferred revenue due to timing differences between billing, cash collection, and revenue recognition. A target with substantial deferred revenue might have limited remaining performance obligations, or vice versa.

Acquirers often value subscription and recurring revenue businesses based partly on deferred revenue balances, viewing them as indicators of contracted future revenue. Under ASC 606, this analysis requires greater sophistication. The remaining performance obligations disclosure provides more relevant information about future contracted revenue, but even this figure requires adjustment for variable consideration constraints and other factors.

7. Judgments and Estimates Create Comparability Challenges

Perhaps most fundamentally, ASC 606 and IFRS 15 introduced substantial judgment into revenue recognition. Identifying performance obligations requires judgment about what constitutes a distinct good or service. Determining transaction prices requires judgment about variable consideration estimates and constraints. Allocating transaction prices requires judgment about standalone selling prices. Recognizing revenue over time requires judgment about appropriate progress measures.

These judgments create comparability challenges that directly affect M&A valuation. Two companies in the same industry with similar business models may reach different conclusions about any of these judgments, producing different revenue recognition outcomes for economically similar transactions. When evaluating a target against comparable transactions or trading multiples, acquirers must consider whether accounting policy differences explain apparent performance differences.

This judgment intensity also creates opportunities. Acquirers may identify targets whose conservative accounting judgments have depressed reported revenue relative to economic substance. Post-acquisition, these acquirers might apply different judgments—within the bounds of GAAP—that enhance reported performance. Conversely, aggressive accounting judgments at the target may require post-acquisition correction, creating negative surprises for unprepared acquirers.

Practical Implications for Deal Execution

Enhanced Due Diligence Requirements

The complexities described above demand enhanced due diligence protocols. M&A professionals should now routinely include ASC 606 compliance in their due diligence scope, covering contract identification procedures, performance obligation identification for significant contracts, transaction price determination including variable consideration estimates, standalone selling price evidence and allocation methods, timing of revenue recognition and progress measures, and contract modification accounting. This analysis should examine not only whether the target’s accounting complies with the standards but also whether reasonable alternative judgments might produce materially different revenue figures.

Purchase Agreement Protections

Purchase agreements should address ASC 606 risks through appropriate representations, warranties, and indemnification provisions. Sellers should represent that their financial statements comply with ASC 606, that their revenue recognition policies have been consistently applied, and that they have provided all material contracts and modifications affecting revenue recognition. Buyers should consider specific indemnification for ASC 606 restatement risk, particularly when acquiring private companies that may have implemented the standards inconsistently.

Earnout Structuring Considerations

Earnouts based on revenue metrics require particular attention to ASC 606 issues. The parties must specify whether earnout revenue will be measured under the target’s historical accounting policies, the acquirer’s policies, or some other defined methodology. Failure to address this question clearly can lead to post-closing disputes when accounting policy differences produce different revenue figures than the parties anticipated.

Integration Planning

Acquirers should include ASC 606 policy alignment in integration planning. If the target’s accounting policies differ from the acquirer’s, post-acquisition harmonization may produce revenue and earnings patterns that differ from pre-acquisition expectations. Understanding these differences before closing allows acquirers to set appropriate expectations with their boards, investors, and other stakeholders.

Conclusion

ASC 606 and IFRS 15 have fundamentally changed the relationship between commercial activity and reported revenue. For M&A professionals, these changes demand new competencies, new due diligence protocols, and new approaches to valuation. The seven areas examined in this article—contract bundling, variable consideration, contract modifications, principal versus agent determinations, timing shifts, deferred revenue interpretation, and accounting judgments—represent the primary channels through which revenue recognition standards affect deal economics.

Mastering these complexities offers significant competitive advantages. Acquirers who understand ASC 606 deeply can identify targets whose conservative accounting has obscured underlying value. Sellers who present clean, well-documented revenue recognition policies command credibility premiums in competitive processes. Advisors who can translate accounting complexity into commercial insight create tangible value for their clients.

The standards themselves will continue to evolve as implementation issues arise and regulators provide additional guidance. The fundamental challenge, however, will remain constant: understanding when revenue is truly what it seems and when the accounting masks different economic reality. For deal professionals willing to engage with these complexities, the rewards—in better valuations, smoother transactions, and fewer post-closing surprises—justify the investment.

As revenue recognition standards continue to mature and new interpretive guidance emerges, how is your organization adapting its M&A due diligence processes to address these evolving challenges?

Leave a comment