Mitsubishi Heavy Industries: How Japan’s Industrial Titan Quietly Built a Global Empire Through Calculated Acquisitions

Mitsubishi Heavy Industries occupies a peculiar position in the global M&A landscape. It is one of the world’s largest and most diversified industrial conglomerates, yet its acquisition strategy rarely commands the same headline attention as, say, a Danaher playbook dissection or a Constellation Software deep dive. That relative obscurity is itself instructive. Where many serial acquirers cultivate a public identity around deal-making velocity, Mitsubishi Heavy Industries has pursued a slower, more deliberate cadence — fewer deals per year, but each one carrying substantial strategic weight. For M&A professionals studying how industrial conglomerates deploy capital across borders, technologies, and business cycles, the Mitsubishi Heavy Industries approach offers a masterclass in patience, vertical integration, and long-horizon thinking.

This article examines Mitsubishi Heavy Industries through the lens that matters most to practitioners: how the company identifies targets, structures transactions, integrates businesses, manages divestitures when theses break down, and positions itself for the next wave of acquisitions. The goal is not hagiography but rigorous analysis — understanding what works, what has stumbled, and what the future likely holds.

The Company: A 140-Year-Old Colossus Still Reinventing Itself

Mitsubishi Heavy Industries, Ltd. (MHI) traces its origins to 1884, when Yataro Iwasaki founded a shipbuilding operation in Nagasaki, Japan. The company formally incorporated under its current name in 1950 after postwar zaibatsu dissolution forced the original Mitsubishi conglomerate to reorganize into separate entities. Today, MHI stands as one of Japan’s largest industrial manufacturers and a Fortune Global 500 mainstay, with consolidated revenues exceeding ¥4.5 trillion (approximately $30 billion) in recent fiscal years.

MHI’s headquarters sit in Tokyo’s Marunouchi district, though the company’s operational footprint extends across the globe. The business operates through four principal segments: Energy Systems, which encompasses gas turbines, nuclear power systems, and environmental equipment; Plant & Infrastructure Systems, covering chemical plants, transportation systems, and bridges; Logistics, Thermal & Drive Systems, which includes turbochargers, engines, forklifts, and air-conditioning equipment; and Aircraft, Defense & Space, spanning fighter jets, launch vehicles, and missile defense platforms.

The company maintains major production facilities across Japan — notably in Nagasaki, Kobe, Hiroshima, Nagoya, and Takasago — alongside manufacturing and engineering sites in the United States, Canada, the United Kingdom, the Netherlands, Singapore, China, India, Brazil, Saudi Arabia, and the Philippines, among others. MHI’s global office network extends to more than 35 countries. The company employs roughly 77,000 people worldwide.

For M&A professionals, the critical structural detail is this: MHI operates across defense, energy, aerospace, and industrial machinery simultaneously. That multi-sector presence creates both extraordinary acquisition optionality and unusual integration complexity. Few companies on earth can credibly evaluate targets ranging from a Florida-based gas turbine services firm to a Swedish rocket propulsion specialist. MHI can — and does.

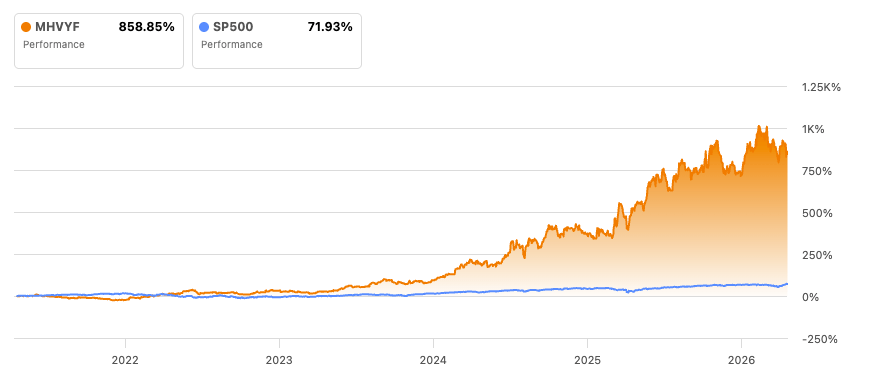

Mitsubishi Heavy Industries (MHVYF) stock performance versus the S&P 500 from 2022 to 2026, showing an approximately 859% return compared to 72% for the broader market — reflecting the market’s growing confidence in MHI’s strategic portfolio shift toward energy transition, defense modernization, and disciplined acquisition-driven growth.

Acquisition History: Strategic Patience Over Deal Volume

Mitsubishi Heavy Industries does not acquire companies at the cadence of a platform-style serial acquirer. Over the past five years, MHI has completed roughly 10 to 15 identifiable acquisitions and strategic equity investments, a figure that looks modest against a Berkshire-style accumulator or a Nordic compounder. In the most recent fiscal year alone, MHI closed a handful of targeted deals, generally in the range of two to five completed transactions. But volume has never been MHI’s game. The company treats acquisitions as precision instruments in service of long-term portfolio reshaping rather than as a flywheel generating compounding returns from deal velocity.

The single largest acquisition in MHI’s modern history — and one of the most consequential industrial transactions in Japan — was the absorption of Mitsubishi Hitachi Power Systems (MHPS) into a wholly owned subsidiary in 2020. MHI acquired Hitachi’s remaining 35% stake in the joint venture for approximately ¥424 billion (roughly $4 billion at the time), consolidating full ownership of what was then the world’s largest gas turbine and thermal power equipment manufacturer. The strategic logic was straightforward: the energy transition demanded that MHI control the full technology roadmap for gas turbines, hydrogen co-firing, carbon capture integration, and digital services, without the governance friction inherent in a joint venture. The deal was renamed Mitsubishi Power and immediately became the backbone of MHI’s energy portfolio.

Beyond that flagship transaction, MHI’s acquisition targets over the past decade reveal a clear thematic pattern. The company consistently pursues targets in three categories:

- Technology and capability bolt-ons: Acquisitions of niche engineering firms, software companies, or component manufacturers that fill specific gaps in MHI’s technology stack. Examples include deals in digital simulation, AI-based predictive maintenance, and advanced materials.

- Geographic market access: Transactions designed to establish or deepen MHI’s presence in high-growth markets. Acquisitions and joint ventures in Southeast Asia, India, and the Middle East for power generation, desalination, and infrastructure services fit this pattern.

- Vertical integration and supply chain control: Deals that bring critical subsystems or aftermarket services in-house, reducing dependency on third-party suppliers and capturing higher-margin recurring revenue streams.

This pattern aligns tightly with MHI’s publicly stated “2021 Business Plan” and its subsequent medium-term strategies, which have progressively shifted the company’s center of gravity toward energy transition technologies, defense modernization, and digital industrial services. MHI’s leadership has been explicit that acquisitions serve these three strategic pillars — and that deals outside those corridors will not be pursued regardless of financial attractiveness.

One observable trend deserves special attention: MHI has increasingly favored acquiring companies with recurring revenue models, particularly in aftermarket services and long-term maintenance contracts. This mirrors a broader industrial trend (GE Vernova, Siemens Energy, and others have pursued similar logic), but MHI’s execution reflects a distinctly Japanese emphasis on relationship continuity. The company tends to acquire service businesses where existing customer relationships are deep and contractually durable, minimizing post-acquisition revenue risk

Acquisition Methods: How MHI Structures and Finances Its Deals

Mitsubishi Heavy Industries employs a range of transaction structures, and the specific approach tends to vary by deal context rather than following a single rigid template.

For large-scale transactions — the MHPS consolidation being the clearest example — MHI has used negotiated bilateral purchases, often acquiring minority stakes from joint venture partners at valuations determined through extended private negotiation rather than competitive auction. This reflects MHI’s deep network of existing partnerships and its preference for deals where relational trust reduces execution risk. Many of MHI’s largest acquisitions over the decades have originated from existing joint ventures or long-standing commercial relationships that naturally evolved into full ownership.

For smaller bolt-on acquisitions, MHI typically engages in privately negotiated transactions with founder-owned or privately held technology companies. The company has also participated in structured carve-outs, purchasing business units from larger conglomerates looking to streamline their own portfolios. MHI has occasionally used competitive auction processes for mid-market targets, though the company’s culture tends to favor proprietary deal flow over contested bidding.

On the financing side, MHI funds acquisitions primarily through a combination of internally generated cash flow and corporate debt facilities. The company maintains investment-grade credit ratings (A-range from major agencies) and has access to deep yen-denominated and dollar-denominated debt markets. MHI has not historically relied on equity issuances to fund acquisitions, preferring to maintain balance sheet discipline and avoid dilution. The company’s net debt-to-equity ratio has generally remained conservative by heavy-industrial standards, typically in the 0.4x to 0.7x range, which provides meaningful headroom for larger transactions when opportunities arise.

Regarding financial advisory relationships, MHI has worked with several of Japan’s leading investment banks and global advisory firms over the years. Nomura Securities and Mizuho Securities have historically served as frequent advisors on domestic transactions and cross-border deals involving Japanese counterparties. For larger international transactions, MHI has engaged global bulge-bracket firms including Goldman Sachs, Morgan Stanley, and JPMorgan, depending on the sector and geography involved. The company does not appear to maintain a single exclusive advisory relationship, instead selecting advisors based on sector expertise and geographic relevance for each specific transaction. This pragmatic approach to advisor selection is consistent with MHI’s broader deal philosophy: each transaction is treated as a distinct strategic event rather than a routine operational function.

Post-Merger Integration: The Quiet Discipline Behind the Deals

Post-merger integration at Mitsubishi Heavy Industries reflects the company’s broader organizational culture: methodical, process-driven, and — by Western M&A standards — notably patient.

MHI maintains internal integration management capabilities embedded within its corporate strategy and business development divisions. The company does not operate a standalone, publicly branded “integration office” in the manner of some U.S. and European serial acquirers (Danaher’s DBS office or Fortive’s FBS team, for example). Instead, MHI assigns integration leadership to senior executives within the acquiring business segment, supported by cross-functional teams drawn from corporate planning, finance, HR, IT, and legal.

This decentralized integration model has practical implications. For deals within MHI’s core domains — energy systems, turbochargers, HVAC equipment — the company’s deep operational expertise allows integration teams to move quickly on supply chain rationalization, engineering standards harmonization, and back-office consolidation. For acquisitions in newer adjacencies, such as digital technology or advanced analytics, MHI has adopted a lighter-touch integration approach, preserving the acquired company’s operational autonomy while gradually aligning on reporting, compliance, and strategic planning cycles.

MHI has engaged external integration advisors on select transactions, particularly for large cross-border deals where cultural integration and organizational design require specialized expertise. Major management consulting firms — McKinsey, Boston Consulting Group, and Deloitte — have reportedly supported MHI on integration planning and execution in various capacities. However, MHI does not appear to maintain a standing retainer with any single integration advisory firm, instead engaging external support on a deal-by-deal basis as complexity warrants.

One integration challenge that M&A professionals should note is the cultural dimension of MHI’s cross-border deals. Japanese industrial acquirers, MHI included, have historically taken a more deliberate and consensus-oriented approach to integration than their American or European counterparts. Decision-making timelines tend to be longer. Organizational restructuring moves at a pace that prioritizes workforce stability and relationship preservation. This approach reduces short-term disruption but can delay synergy realization. Whether that trade-off is positive or negative depends entirely on the time horizon one applies — and MHI’s time horizon, shaped by 140 years of institutional history, is considerably longer than a typical private equity hold period.

Divestitures: Knowing When to Walk Away

Not every acquisition thesis proves correct, and not every business unit remains strategically relevant forever. Mitsubishi Heavy Industries has demonstrated a willingness — sometimes reluctant, sometimes decisive — to divest businesses that no longer fit its evolving portfolio strategy.

The most significant divestiture in MHI’s recent history was the exit from the commercial aircraft business through the effective wind-down of the Mitsubishi SpaceJet program (formerly known as the Mitsubishi Regional Jet, or MRJ). While technically not a divestiture in the traditional M&A sense — MHI did not sell the program to a third party — the 2023 decision to formally terminate the SpaceJet development program after more than $10 billion in cumulative investment represented the single largest strategic write-off in the company’s modern history. The program had suffered repeated certification delays, design changes, order cancellations, and cost overruns over more than a decade. MHI’s leadership ultimately concluded that the commercial regional jet market did not offer a viable path to profitability given the competitive dynamics dominated by Embraer and the Airbus-Boeing duopoly. The decision was painful but strategically rational: it freed up engineering resources and capital for defense aviation, space launch systems, and energy transition investments with clearer return profiles.

Beyond the SpaceJet wind-down, MHI has executed smaller divestitures and portfolio pruning exercises over the years. The company sold its forklift business (Mitsubishi Forklift Trucks, under the Mitsubishi Logisnext brand) through strategic restructurings and explored options for non-core industrial units that lacked sufficient scale or strategic alignment. MHI has also exited selected joint ventures in markets where competitive dynamics shifted unfavorably.

The strategic reasoning behind MHI’s divestitures consistently follows a portfolio logic: the company aims to concentrate resources on businesses where it holds genuine global-scale competitive advantage and where long-term demand tailwinds are strongest. Businesses that fail either test — lacking competitive differentiation or facing structural demand headwinds — become divestiture candidates, regardless of their historical significance to the company.

MHI has not publicly disclosed a preferred divestiture or carve-out advisory firm. Given the company’s advisory approach on the acquisition side, it likely selects divestiture advisors based on transaction-specific criteria. For complex carve-outs involving cross-border operations, global investment banks with strong M&A execution capabilities and Japanese market knowledge (Nomura, Goldman Sachs, Morgan Stanley) would be logical choices.

The Future: Where Will MHI Acquire Next?

Predicting specific acquisition targets is a fool’s errand, but predicting the strategic corridors in which MHI will hunt is a considerably more tractable exercise. Three themes will almost certainly define MHI’s acquisition agenda over the next five to ten years.

Energy transition technology will remain the dominant acquisition theme. MHI has publicly committed to developing hydrogen-fired gas turbines, carbon capture and storage (CCS) solutions, and next-generation nuclear technologies (including small modular reactors). The company will likely acquire or invest in companies that accelerate its capabilities in hydrogen production and storage, CO₂ transport and sequestration, advanced nuclear fuels and reactor components, and grid-scale energy storage. Targets in North America, Europe, and Australia — where CCS and hydrogen ecosystems are most advanced — will be particularly attractive. Expect MHI to pursue a mix of minority equity stakes in early-stage technology companies and full acquisitions of proven, commercially operational businesses.

Defense and space will be the second major acquisition corridor. Japan’s historic decision in late 2022 to dramatically increase defense spending — doubling the defense budget to approximately 2% of GDP by 2027 — creates a structural demand tailwind for MHI, which is Japan’s largest defense contractor. MHI will likely seek acquisitions that enhance its capabilities in missile defense systems, autonomous platforms, cybersecurity, space situational awareness, and satellite systems. Cross-border defense acquisitions are complicated by national security regulations (CFIUS in the U.S., equivalent regimes in Europe), but MHI may pursue partnerships, joint ventures, or minority investments that provide technology access without triggering regulatory barriers.

Digital and industrial software represents the third acquisition frontier. MHI has been investing in AI, digital twins, predictive maintenance platforms, and industrial IoT through its “ENERGY CLOUD” and “Orizuru” digital initiatives. The company will likely acquire niche software companies and data analytics firms that can integrate into MHI’s installed base of gas turbines, compressors, HVAC systems, and other equipment. These acquisitions will tend to be smaller in transaction value but high in strategic significance, enabling MHI to shift toward outcome-based service models and recurring revenue streams.

One wildcard factor is MHI’s potential role in industry consolidation within Japan’s broader industrial sector. Japan’s demographic decline and corporate governance reforms are accelerating portfolio restructuring across the country’s major conglomerates. MHI could emerge as a consolidator, acquiring business units divested by companies like Toshiba, Hitachi, or IHI as those firms continue their own portfolio transformations. The Hitachi Power Systems transaction established a precedent for exactly this type of deal.

From a financial capacity standpoint, MHI is well-positioned for a more aggressive acquisition phase. The company’s operating cash flows have strengthened materially in recent years, driven by energy systems demand and defense order growth. MHI’s balance sheet retains meaningful debt capacity, and the company’s improved profitability profile reduces the execution risk associated with larger transactions.

Conclusion: The Long Game in an Impatient World

Mitsubishi Heavy Industries will never top a league table for deal count. The company’s acquisition strategy is not designed for that purpose. Instead, MHI exemplifies an approach that prizes strategic coherence over transaction volume, long-term capability building over short-term multiple arbitrage, and integration patience over rapid synergy extraction.

For M&A professionals, MHI offers a valuable counterpoint to the dominant Anglo-American serial acquirer model. The company demonstrates that disciplined, infrequent acquisitions — executed within a clear strategic framework and supported by deep operational expertise — can generate durable competitive advantage across decades, not just quarters. The MHPS consolidation alone reshaped global power generation competition in ways that will reverberate for years.

At the same time, the SpaceJet debacle is a sobering reminder that even the most capable industrial acquirers can misjudge the difficulty of entering new markets through internal development. That failure arguably strengthened MHI’s acquisition discipline by reinforcing the lesson that buying proven capabilities often beats building them from scratch.

As the energy transition accelerates, defense spending surges, and digital transformation reshapes industrial business models, MHI sits at the intersection of multiple secular growth trends with the financial firepower and strategic clarity to act. The question is not whether MHI will acquire — it is whether the company will move quickly enough to capture opportunities before faster-moving competitors close the window.

Given MHI’s 140-year track record of strategic patience, should we bet on the company accelerating its acquisition pace — or trust that slow and steady will continue to win this particular race?

Leave a comment