The M&A Rearview Mirror: How Look-Back Analysis on Synergy Forecasts Transforms Your Deal Playbook

Every M&A team has a filing cabinet — physical or digital — stuffed with board presentations that once projected bold synergy numbers. Revenue uplift of 15% within three years. Cost savings of $200 million by year two. Procurement synergies alone worth $50 million annually. Those projections justified premium valuations, rallied stakeholder support, and unlocked deal approvals. But how many of those same teams ever returned to those projections, years later, with an honest spreadsheet and an open mind?

Surprisingly few. Research consistently shows that between 60% and 80% of mergers fail to deliver their anticipated synergies in full, yet the majority of acquirers never conduct a systematic comparison of forecasted synergies against actual results. The integration closes, the deal team disperses, the next transaction lands on the desk, and the institutional memory of what was promised versus what materialized quietly fades. This pattern represents one of the most significant missed opportunities in corporate development.

A disciplined “look-back” analysis — the structured, post-hoc comparison of synergy forecasts with realized outcomes — can break this cycle. It transforms past deals from closed chapters into living data sets that sharpen future due diligence, recalibrate valuation models, and strengthen integration execution. For serial acquirers operating across geographies and sectors, this retrospective discipline becomes a compounding advantage, one that separates organizations that learn from their deals from those that merely repeat them.

This article explores what a look-back analysis is, how to conduct one rigorously, and why the insights it yields are among the most valuable upgrades an M&A team can make to its playbook. Along the way, we will examine three real-world examples of companies that have embraced this discipline — and reaped tangible benefits from doing so.

Defining the Core Concepts

What Is a “Look-Back” Analysis?

A look-back analysis is a structured, retrospective evaluation that compares the synergy projections made during the deal approval phase with the actual financial and operational outcomes achieved post-integration. It is not an audit in the compliance sense, nor is it a blame exercise. It is an analytical discipline designed to extract learning from experience.

At its core, the analysis asks three deceptively simple questions: What did we forecast? What actually happened? Why did the two diverge?

The first question requires retrieving the original synergy models, board memoranda, and integration business cases. The second demands clean post-merger financial data, often requiring isolation of the acquired business’s contribution from organic performance — a task that grows harder the longer the analysis is delayed. The third question is where genuine insight lives, because the reasons for divergence — whether rooted in flawed assumptions, integration missteps, market shifts, or overly conservative estimates — are what inform future improvement.

What Are Synergy Forecasts, and Why Do They Matter So Much?

For those who live in the M&A world, synergies need little introduction, but precision in definition matters here because imprecision is often where forecasting errors begin. Synergies are the incremental value created by combining two businesses that neither could achieve independently. They typically fall into three categories:

- Cost synergies represent savings from eliminating redundancies, consolidating facilities, renegotiating supplier contracts, and streamlining overhead. These are generally the most predictable and the first to be realized.

- Revenue synergies capture the additional top-line growth expected from cross-selling, expanded market access, combined product portfolios, or enhanced pricing power. These are notoriously harder to forecast and slower to materialize.

- Financial synergies include benefits such as a lower cost of capital, tax optimization, and improved balance sheet efficiency. These tend to be more technical and often overlooked in integration tracking.

Synergy forecasts underpin the financial justification for nearly every acquisition. They determine the maximum price a buyer should pay, they shape the integration thesis, and they set the expectations against which management will ultimately be judged. When those forecasts are systematically disconnected from reality — and no one examines why — the organization is effectively flying blind on every subsequent deal.

The M&A Playbook: A Living Document That Should Evolve

An M&A playbook is the codified set of processes, frameworks, templates, and institutional knowledge that guides an organization through the deal lifecycle, from target identification and due diligence through negotiation, integration planning, and post-merger value capture. Mature acquirers maintain detailed playbooks that cover governance structures, integration management office design, functional workstream checklists, communication protocols, Day 1 readiness plans, and synergy tracking methodologies.

The critical word in that description is “living.” A playbook that remains static after each deal fails to absorb the lessons that only execution can teach. The look-back analysis is the mechanism through which those lessons are identified, quantified, and fed back into the playbook so that each subsequent deal benefits from the accumulated wisdom of every prior one.

Current Trends Driving Interest in Look-Back Discipline

Several converging forces are pushing look-back analysis higher on the corporate development agenda. Boards and investors are demanding greater accountability for deal outcomes, particularly after a decade of elevated multiples and, in many cases, disappointing post-merger returns. Private equity sponsors, who have always been more disciplined about tracking value creation, are raising the bar for corporate acquirers. ESG integration adds new dimensions of synergy and risk that lack historical benchmarks, making retrospective calibration even more important. And the growing availability of advanced analytics and integration management platforms makes the mechanics of tracking and comparing forecasts versus actuals more feasible than ever before.

Three Reasons a Look-Back Analysis Creates Transformative Value

Reason 1: It Recalibrates Synergy Estimation Accuracy

The most immediate and quantifiable benefit of a look-back analysis is that it forces an organization to confront its own estimation biases. Every M&A team develops habitual patterns in how it models synergies. Some teams chronically overestimate revenue synergies because they underweight customer attrition risk. Others systematically undercount integration costs, treating them as one-time charges that somehow never appear in the final tally. Some are too conservative on procurement savings because they lack visibility into the target’s supplier contracts during diligence.

A look-back analysis surfaces these patterns with data rather than anecdote. When a corporate development team reviews five or ten past deals and discovers that revenue synergies were achieved at only 40% of forecast while cost synergies came in at 110%, it gains a powerful calibration tool. Future models can apply empirically derived “realization rates” to different synergy categories, geographies, and deal types. The team can also identify which specific line items within each synergy category are most prone to overestimation or underestimation.

This recalibration directly impacts several elements of the M&A playbook. Valuation models and maximum bid calculations become more reliable. Sensitivity analyses become grounded in actual variance ranges rather than hypothetical scenarios. Due diligence checklists expand to probe the areas where past forecasts have proven weakest. The synergy estimation templates themselves can be restructured to require more granular assumptions and explicit risk-adjustment factors for each line item.

Importantly, this recalibration is not about becoming more conservative across the board. In some cases, look-back analyses reveal that certain synergy categories were consistently underestimated, meaning the organization was leaving value — and potentially attractive deals — on the table.

Reason 2: It Strengthens Integration Planning and Execution

Synergy shortfalls are rarely caused by bad arithmetic alone. More often, the gap between forecast and actual reflects breakdowns in integration execution: delays in system migration, cultural resistance to organizational restructuring, talent attrition in critical functions, or underinvestment in integration resources. A look-back analysis that goes beyond the numbers to examine the operational narrative behind each variance becomes a diagnostic tool for integration effectiveness.

Consider what a thorough look-back reveals about integration timelines. If an organization consistently finds that cost synergies required 18 months to achieve rather than the modeled 12, the playbook’s integration planning templates need to adjust phasing assumptions. If revenue synergies repeatedly stalled because sales teams were not trained on the combined product portfolio until six months post-close, the playbook’s Day 1 readiness checklist and first-100-days plan need to pull that workstream forward.

The look-back also illuminates resource allocation patterns. Teams frequently discover that they understaff integration management offices, rely too heavily on line managers who are simultaneously running the business, or fail to dedicate sufficient budget to change management and internal communication. These patterns, once identified, translate directly into updated resource planning templates and governance structures within the playbook.

Cultural integration — often cited as the leading cause of merger failure — is another area where retrospective analysis proves invaluable. By interviewing key participants from past deals and correlating their experiences with synergy outcomes, organizations can develop more nuanced cultural assessment frameworks for future diligence. They can also identify which cultural integration interventions (joint leadership workshops, cross-functional project teams, unified incentive structures) correlated with stronger outcomes and codify those into the playbook.

Reason 3: It Builds Institutional Memory and Organizational Accountability

M&A teams are inherently transient. Deal leads rotate, integration managers move on, and the executives who championed a transaction may be in different roles — or different companies — by the time results are measurable. Without a formal look-back process, the lessons from each deal walk out the door with the individuals who lived them.

A structured look-back analysis converts personal experience into organizational knowledge. When its findings are documented, discussed in cross-functional reviews, and embedded into updated playbook content, they create a durable institutional asset. New team members can review the look-back reports from prior deals to understand the organization’s M&A track record, its typical pitfalls, and its proven success factors. This onboarding value alone can accelerate the effectiveness of new hires by months.

The accountability dimension is equally powerful. When everyone involved in a deal knows that a rigorous look-back will be conducted two to three years after close, the quality of upfront forecasting tends to improve. Deal champions become more disciplined about distinguishing between base-case and stretch synergies. Integration leaders take ownership of synergy tracking from Day 1 rather than treating it as a finance exercise that happens in the background. Board presentations include more realistic ranges and explicit assumptions rather than single-point estimates designed to clear the approval hurdle.

This cultural shift — from “forecast to win approval” to “forecast to create accountability” — is perhaps the most enduring benefit a look-back discipline can produce. It reshapes the incentive structure around deal-making in subtle but profound ways.

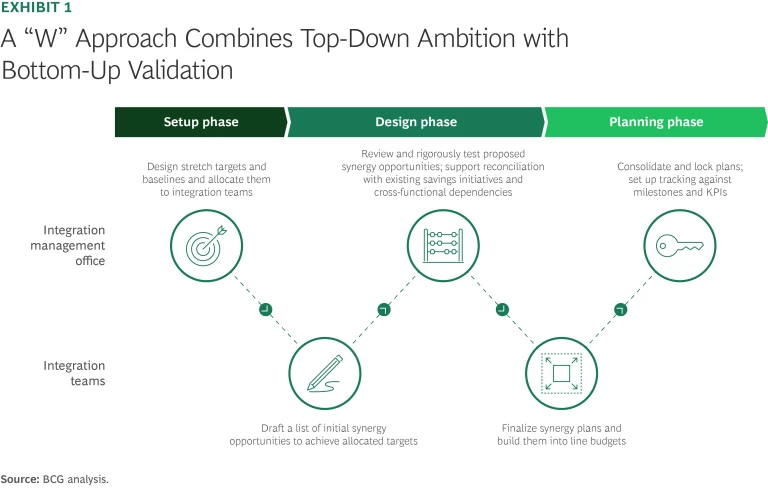

How to Perform a Look-Back Analysis: A Practical Framework

For teams ready to implement this discipline, the following framework provides a structured approach:

Step 1: Assemble the baseline. Retrieve the original synergy models, investment committee memoranda, board presentations, and integration plans for each deal under review. Document the specific synergy projections by category, magnitude, and projected timeline.

Step 2: Gather actual performance data. Collect post-merger financial data for the relevant periods, ideally spanning three to five years post-close. Work with finance teams to isolate the acquired business’s contribution and, where possible, attribute specific performance changes to integration actions versus organic or market-driven factors.

Step 3: Conduct the variance analysis. Compare forecasted synergies against actuals by category, timeline, and magnitude. Calculate realization rates for each synergy type and identify patterns across deals (by deal size, geography, sector, and synergy category).

Step 4: Investigate root causes. For each material variance — positive or negative — investigate the underlying drivers. Conduct interviews with deal team members, integration leaders, and functional heads. Review integration tracking reports, milestone completion records, and post-merger organizational changes.

Step 5: Synthesize findings and update the playbook. Translate the analysis into specific, actionable playbook updates. These may include revised synergy estimation templates with empirically derived realization haircuts, updated due diligence checklists that probe previously underexamined areas, refined integration timelines and resource models, improved cultural assessment frameworks, and enhanced synergy tracking protocols for future deals.

Step 6: Institutionalize the process. Establish a recurring look-back cadence — typically at the two-year and five-year marks post-close — and assign clear ownership for conducting the analysis and implementing playbook updates. Incorporate look-back findings into corporate development team training and onboarding materials.

What If Synergies Were Never Tracked?

A practical question arises: can a look-back analysis be performed if the organization never formally tracked synergies on previous deals? The answer is yes, though with caveats.

Even without a dedicated synergy tracking system, the building blocks for a retrospective assessment usually exist. The original deal model and board presentation provide the forecast baseline. Post-merger financial statements, management accounts, and segment reporting provide actual performance data. Interviews with integration leaders and functional heads can reconstruct the operational narrative.

The analysis will be less precise and will require more judgment calls about attribution — separating synergy-driven improvements from organic trends, market movements, and unrelated management actions. However, even an imperfect look-back that identifies directional patterns (for example, “we consistently overestimate revenue synergies in cross-border deals”) is vastly more useful than no look-back at all. The exercise also serves as a powerful catalyst for establishing formal synergy tracking protocols on all future deals, closing the data gap for the next retrospective cycle.

Three Real-World Examples of Look-Back Discipline in Action

Example 1: Danaher Corporation — The Perpetual Learning Machine

Danaher Corporation, the diversified industrial conglomerate, has built one of the most admired acquisition track records in corporate history, completing over 400 acquisitions since the 1980s. Central to Danaher’s approach is the Danaher Business System (DBS), a rigorous operating methodology rooted in continuous improvement principles that the company applies to every acquired business.

Danaher’s post-acquisition reviews are deeply embedded in its operating cadence. The company systematically evaluates the performance of each acquisition against its original investment thesis, including synergy and operational improvement targets. These reviews are not one-time events but recurring assessments that track value creation over multiple years. The findings feed directly back into how Danaher screens targets, structures diligence, and designs integration plans.

The result of this discipline is visible in Danaher’s synergy estimation accuracy, which has improved over successive deal waves. The company has refined its understanding of which types of operational improvements are achievable within specific timeframes for businesses of different sizes, in different industries, and at different stages of operational maturity. This empirically grounded knowledge allows Danaher to bid with confidence, avoid overpaying for speculative synergies, and consistently extract value from its acquisitions. Danaher demonstrates that look-back analysis, when embedded in the corporate operating system rather than treated as an occasional exercise, becomes a self-reinforcing competitive advantage.

Example 2: Kraft Heinz — Learning from a Painful Reckoning

The 2015 merger of Kraft Foods and H.J. Heinz, orchestrated by 3G Capital and Berkshire Hathaway, initially appeared to be a synergy success story. The combined company exceeded its original $1.5 billion cost synergy target ahead of schedule, largely through aggressive zero-based budgeting and headcount reductions. However, the longer-term picture told a different story.

By 2019, Kraft Heinz had written down the value of its brands by over $15 billion, acknowledging that the relentless cost-cutting had hollowed out brand investment, product innovation, and growth capacity. Revenue synergies never materialized in meaningful form. The company’s retrospective assessment — forced in part by the scale of the write-downs and subsequent SEC investigation — revealed that the original synergy thesis had been dangerously one-dimensional. Cost synergies had been treated as the entire value creation story, while revenue sustainability and brand health had been insufficiently modeled and monitored.

Kraft Heinz’s experience became a widely studied cautionary case across the consumer goods and broader M&A communities. It underscored a critical lesson that look-back analysis can surface: achieving cost synergies at the expense of revenue-sustaining capabilities can destroy more value than it creates. The company subsequently restructured its approach to acquisitions and portfolio management, placing greater emphasis on growth investment and brand stewardship. For other acquirers, Kraft Heinz’s experience serves as a powerful argument for look-back analyses that evaluate the full spectrum of synergy outcomes — including the second-order effects of synergy capture strategies on long-term business health.

Example 3: Illinois Tool Works (ITW) — Codifying Decades of Acquisition Learning

Illinois Tool Works, the diversified manufacturer with a portfolio built through hundreds of acquisitions, provides an example of how look-back insights can reshape not just deal-making but an entire corporate strategy. Over decades of acquisitive growth, ITW accumulated extensive data on which types of acquisitions consistently delivered expected returns and which did not.

In 2012, ITW launched its “Enterprise Strategy,” a fundamental restructuring that consolidated its more than 800 operating divisions into roughly 85 divisions organized around core segments. This strategic pivot was informed in significant part by retrospective analysis of its acquisition and operating track record. ITW’s leadership recognized, through systematic review, that smaller bolt-on acquisitions within core segments produced more reliable synergy capture and return on invested capital than larger, more diversified deals. The company also identified that its decentralized operating model, while fostering entrepreneurship, sometimes hindered the realization of cross-business synergies.

These look-back-informed insights led ITW to refine its M&A playbook in fundamental ways. The company narrowed its acquisition focus to high-quality businesses in core segments, raised the bar on synergy validation during diligence, and redesigned its integration approach to balance operational autonomy with synergy capture. The results have been striking: ITW’s operating margins expanded from approximately 15% to over 25% in the years following the strategy shift, and the company’s return on invested capital improved significantly. ITW’s experience demonstrates that look-back analysis can deliver value far beyond incremental playbook refinements — it can catalyze strategic transformation.

Conclusion

The look-back analysis occupies a peculiar position in the M&A landscape. Almost every experienced practitioner acknowledges its value. Almost every academic study on deal performance recommends it. Yet the majority of organizations still do not perform it with any rigor or regularity. The reasons are understandable — deal teams are forward-looking by nature, integration is exhausting, attribution is messy, and revisiting past forecasts can be politically uncomfortable. None of these reasons is good enough.

The evidence from organizations like Danaher, Kraft Heinz, and ITW demonstrates that systematic retrospective analysis of synergy forecasts versus actuals produces tangible, compounding benefits. It sharpens estimation accuracy, strengthens integration execution, builds institutional memory, and creates a culture of accountability that elevates the quality of every future transaction. For serial acquirers operating in complex global markets, these benefits are not incremental improvements — they are foundational capabilities.

The M&A playbook is only as good as the feedback loops that refine it. A look-back analysis is the most powerful feedback loop available, and its cost — a few weeks of analytical work and some honest conversations — is trivial relative to the billions of dollars riding on the next deal’s synergy assumptions.

So here is the question worth sitting with: if your organization has completed multiple acquisitions over the past decade, how confident are you that the synergy assumptions in your next deal reflect what you have actually learned — rather than what you have merely hoped?

Leave a comment