Stress-Testing the Upside: Why Synergy-Case Sensitivity Analysis Dictates M&A Investment Success

Corporate history overflows with acquisitions that looked magnificent on a spreadsheet but crumbled during post-merger integration. Investment banking pitch books famously present synergy curves that resemble pristine, upward-sloping Alpine peaks. Yet, experienced corporate development leaders know that the actual path to integration looks much more like a treacherous mountain pass filled with unexpected delays and steep costs. Why does this discrepancy between modeled expectations and operational reality persist?

The systemic failure of many corporate marriages rarely stems from a lack of talent or flawed baseline operations. Instead, it occurs because deal teams frequently treat synergy assumptions as a deterministic certainty rather than a volatile, probabilistic distribution. When an acquisition relies heavily on synergy realization to justify a hefty premium, a failure to stress-test those assumptions introduces catastrophic risk to the buyer’s balance sheet.

This long-form analysis explores how synergy-case sensitivity analysis transforms speculative investment theses into rigorous, risk-adjusted strategic roadmaps. For seasoned mergers and acquisitions (M&A) professionals operating in volatile global markets, this analytical tool provides the ultimate guardrail against strategic overconfidence. How can dealmakers accurately separate genuine value creation from spreadsheet illusions? The answer lies in the disciplined application of multi-variable sensitivity modeling.

Demystifying the Core Themes: Risk, Synergies, and Market Realities

To appreciate the strategic utility of advanced sensitivity modeling, practitioners must first establish a uniform vocabulary around deal risk and value creation. A common language ensures that corporate development teams, executive boards, and private equity sponsors evaluate investment opportunities through the same objective lens.

Defining the Investment Thesis and Risk Exposure

An investment thesis serves as the foundational argument for allocating capital to a specific corporate acquisition. It outlines the strategic rationale, market opportunities, and financial mechanisms that will generate superior returns compared to the companies operating independently.

Risk exposure represents the quantifiable vulnerability of this investment thesis to internal execution failures and external macroeconomic shocks. In an institutional context, deal teams calculate risk exposure by measuring the variance between the projected net present value (NPV) of a transaction and its actual realized financial outcomes. High risk exposure indicates that minor deviations from the baseline operational model will disproportionately destroy investor capital.

The Anatomy of Synergy-Case Sensitivity Analysis

What exactly is a synergy-case sensitivity analysis? It is a financial stress-testing methodology that isolates specific synergy assumptions and evaluates how variances in their timing, magnitude, and cost to achieve alter the transaction’s ultimate financial return.

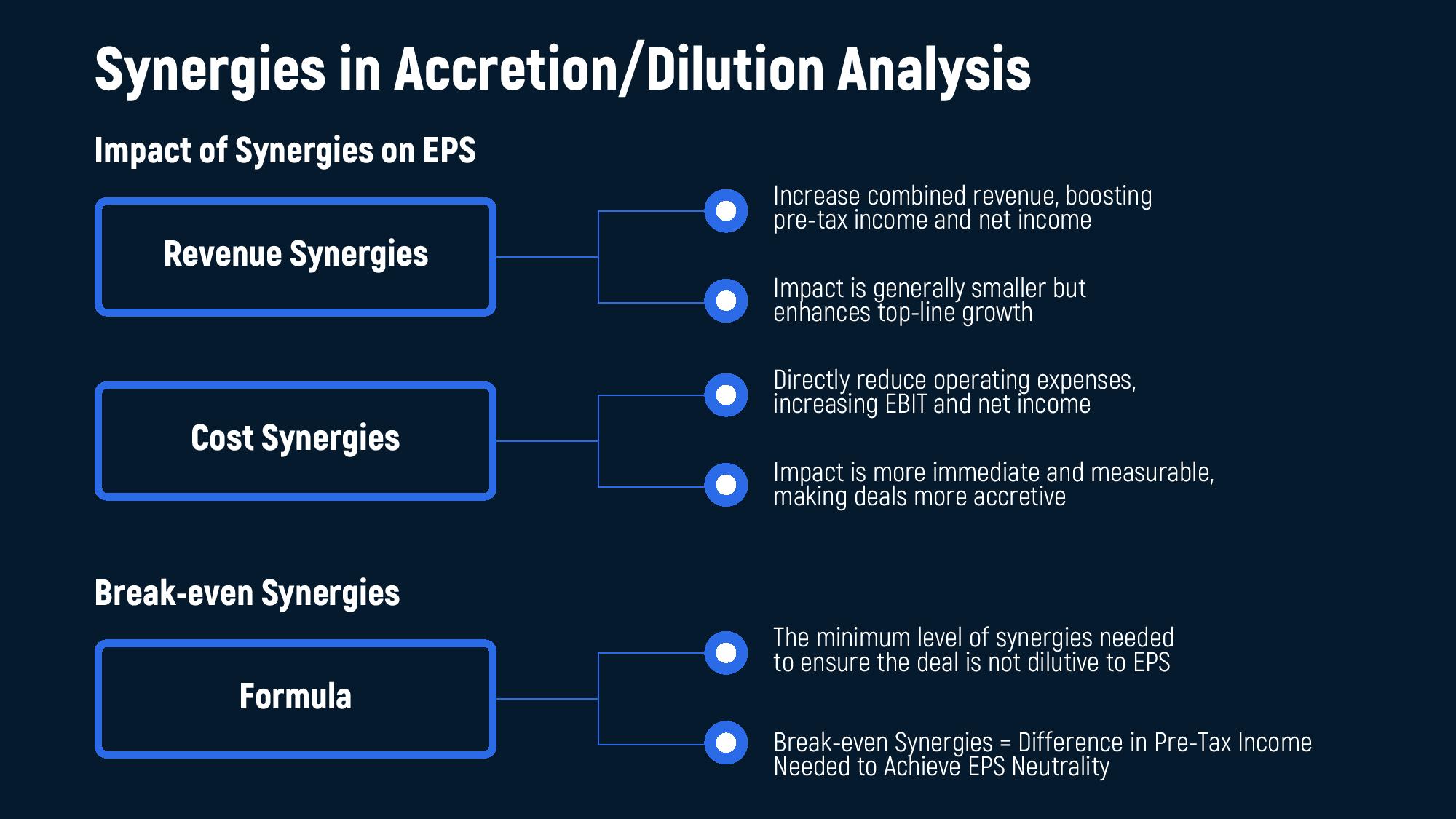

Unlike a standard operational sensitivity analysis, which alters baseline revenue growth or cost of goods sold, this specific framework focuses exclusively on the incremental value created by combining the two corporate entities. The analysis isolates cost synergies, such as headcount reductions and procurement savings, alongside revenue synergies, such as cross-selling products and geographic expansion. By manipulating these variables independently and concurrently, analysts expose the precise points where the transaction ceases to be financially viable.

Current Trends Shaping Global M&A Dynamics

The necessity of rigorous sensitivity modeling has accelerated due to structural changes in the global macroeconomic landscape. Several prominent trends now dictate how corporate development teams underwrite transaction risk:

- Elevated Cost of Capital: Higher global interest rates mean that deal financing requires greater debt service obligations and elevated hurdle rates.

- Aggressive Regulatory Scrutiny: Antitrust regulators globally are delaying closing timelines, which directly defers the realization of operational efficiencies.

- Compressed Operational Margins: Global inflationary pressures make cost-saving assumptions harder to sustain over a multi-year integration horizon.

Because cheap capital can no longer cover up integration delays, precision in underwriting has become the primary differentiator between value creation and capital destruction. Corporate boards now demand detailed proof that an acquisition can withstand integration friction without violating debt covenants.

The Blueprint for Quantifying Risk Exposure

Assessing risk exposure within an investment thesis requires moving away from qualitative intuition and embracing structured, quantitative frameworks. Seasoned dealmakers look at a target business not as a static entity, but as a collection of dynamic, interconnected risk vectors.

To execute a comprehensive risk assessment, the deal team must categorize vulnerabilities into three operational domains:

- Macroeconomic sensitivities track variables outside management’s immediate sphere of influence, including currency fluctuations, regional interest rates, and shifting trade regulations.

- Core standalone target risks evaluate the underlying operational stability of the acquired business, such as customer churn rates, technological obsolescence, and key talent retention.

- Synergy execution risks measure the operational friction associated with combining two distinct corporate structures, including cultural misalignments, IT system incompatibilities, and supply chain disruptions.

How can a synergy-case sensitivity analysis help assess risk exposure in an investment thesis? It connects these abstract risk categories directly to the valuation model. By varying synergy inputs while keeping standalone operational assumptions constant, the analyst isolates the exact financial impact of integration failures.

The analytical workflow follows a direct sequential path. The corporate development team establishes the investment thesis baseline. Analysts apply the synergy-case sensitivity framework directly to that baseline. This process allows the team to isolate the valuation impact by simultaneously altering three levers: the synergy timing, the synergy magnitude, and the explicit cost to achieve.

This modeling technique allows the corporate development team to identify the deal’s exact breaking point. For instance, the analysis might reveal that a six-month delay in consolidating manufacturing facilities completely erodes the transaction’s projected internal rate of return (IRR). Armed with this granular data, executive committees can make informed decisions regarding capital allocation rather than relying on optimistic management projections.

Mechanics of Constructing a Robust Sensitivity Framework

Performing a good synergy-case sensitivity analysis requires a sophisticated, systematic approach that goes far beyond simply dropping a generic “downside case” into a financial model. The process demands a deep partnership between the corporate development team, the commercial due diligence consultants, and the post-merger integration leads.

An institutional-grade analysis demands a structured, multi-dimensional framework:

1. Deconstruct Synergies into Discrete, Auditable Line Items

Analysts must avoid grouping all cost savings into a single, amorphous line item on the spreadsheet. The deal team must break down every projected synergy into its core operational component. Procurement savings must be separated by supplier category. Headcount reductions must be categorized by department and geographic region. Revenue cross-selling must be modeled by specific product lines and target customer segments. This level of granularity allows for the assignment of unique risk profiles to each distinct value driver.

2. Apply Realistic Time-Phasing and Realization Curves

Synergies do not materialize instantaneously upon the closing of a transaction. A robust model maps out realistic realization curves over a multi-year horizon, typically spanning three to five years. The framework must account for the reality that cost synergies achieve scale much faster than revenue synergies. While a corporate headquarters can be consolidated within the first twelve months, cross-selling a specialized software suite to an entirely new enterprise customer base frequently requires twenty-four to thirty-six months of market cultivation.

3. Factor in the Explicit Cash Costs Required to Achieve Synergies

Every dollar of corporate synergy carries an associated upfront implementation cost. Eliminating redundant facilities requires lease termination penalties and employee severance packages. Harmonizing disparate enterprise resource planning (ERP) platforms requires substantial investments in external IT consultants and software licenses. A precise sensitivity analysis treats these “costs to achieve” as highly volatile variables. The model must explicitly test how an overrun in integration expenses impairs the transaction’s near-term cash flows.

4. Construct Multi-Variable Sensitivity Matrices

The ultimate stage of a sophisticated analysis involves the creation of multi-variable data tables. These matrices test the simultaneous degradation of multiple synergy assumptions to reflect the interconnected nature of real-world integration challenges. The framework below outlines the clear operational distinctions between baseline deterministic sensitivity modeling and advanced probabilistic modeling:

Deterministic Sensitivity Modeling

- Variable Manipulation: Changes one or two variables at a time using fixed, static increments.

- Output Characteristics: Generates a rigid grid of outcomes showing specific valuation points.

- Handling of Variable Interaction: Ignores the compounding effect of concurrent operational failures.

- Strategic Application: Provides quick baseline boundaries for initial transaction screening.

Advanced Probabilistic Modeling

- Variable Manipulation: Manipulates dozens of variables simultaneously using randomized distributions.

- Output Characteristics: Produces a probability distribution curve outlining the likelihood of success.

- Handling of Variable Interaction: Models the systemic correlation between delayed timelines and rising costs.

- Strategic Application: Guides final purchase price negotiations and structures complex earn-out clauses.

By utilizing this comprehensive approach, the investment committee moves away from asking whether a deal is generally good or bad. Instead, they determine the exact probability of achieving the strategic returns promised in the original investment thesis.

Three Uncompromising Reasons Why Synergy-Case Sensitivity Dictates Deal Value

Understanding the mechanical execution of sensitivity modeling is merely a prerequisite. The true value of this analytical discipline lies in how it reshapes strategic decision-making at the highest corporate levels. When deployed effectively, synergy-case sensitivity analysis yields three profound advantages for global dealmakers.

Reason 1: It Exposes the Structural Fragility of the Purchase Price Multiple

Acquirers frequently justify paying premium valuation multiples by factoring assumed synergies directly into the pro-forma EBITDA calculations. For example, a buyer might agree to pay a twelve-times multiple on a target’s $50 million standalone EBITDA because they project $10 million in run-rate synergies, which theoretically drops the effective multiple to a more palatable ten times.

A rigorous synergy-case sensitivity analysis systematically deconstructs this rationale. By stress-testing the magnitude and timing of that extra $10 million, the analysis exposes how easily a minor integration misstep can drive the effective multiple back up to an unsustainable level. This insight protects corporate buyers from the psychological trap of deal momentum, preventing them from overpaying for assets under the mistaken belief that synergies are guaranteed.

Reason 2: It Optimizes Capital Structure Design and Protects Debt Covenants

Leveraged acquisitions rely on steady, predictable post-transaction cash flows to service significant debt burdens. If a deal team models aggressive cost synergies to prove that the combined company can comfortably cover its interest expenses, any shortfall in those savings can jeopardize the firm’s financial stability.

The cascading impact of unexamined assumptions follows a highly destructive path. Aggressive synergy assumptions frequently lead to unexpected integration delays. These delays create an immediate cash flow shortfall for the combined entity. Consequently, this shortfall triggers a deleveraging failure and causes an immediate breach of senior debt covenants.

Conducting a synergy sensitivity analysis allows treasury teams to size debt tranches based on a clear understanding of worst-case scenarios. If the analysis reveals that a 30% shortfall in synergy realization leads to a breach of senior leverage covenants, the Chief Financial Officer can adjust the financing mix accordingly. This proactive step ensures that the company maintains an adequate capital buffer, preserving its credit rating and keeping it out of costly restructuring negotiations.

Reason 3: It Transforms Negotiation Impasses into Structured Earn-Out Mechanisms

M&A negotiations frequently stall because buyers and sellers hold radically different views on the value of future synergies. Sellers want to be compensated today for the future upside they believe their business enables. Buyers, conversely, are reluctant to pay upfront for efficiencies they have yet to achieve.

Synergy-case sensitivity analysis provides the empirical foundation needed to bridge this valuation gap. By mapping out the exact financial impact of different synergy scenarios, the deal team can structure precise earn-out mechanisms. The buyer can agree to pay a higher total price, but only if specific synergy milestones are fully realized over time. This approach shifts execution risk back to the seller, allowing both parties to align on an equitable risk-adjusted transaction structure.

Real-World Manifestations of Sensitivity Analysis in Action

Examining theoretical frameworks provides conceptual clarity, but observing how these principles manifest in real-world global transactions cements their practical value. The following three scenarios illustrate how synergy-case sensitivity analysis shapes commercial outcomes across diverse industries.

Case Scenario 1: The Global Technology Consolidation and Revenue Synergy Lags

A prominent enterprise software conglomerate sought to acquire a high-growth, niche artificial intelligence platform for $1.2 billion. The core investment thesis relied heavily on revenue synergies. The corporate development team projected that the acquirer’s global sales force could rapidly cross-sell the target’s AI tools to its massive existing customer base, generating an additional $150 million in run-rate revenue within twenty-four months.

Revenue synergies look beautiful on a slide deck, but they require rewriting sales incentives, retargeting accounts, and retraining account executives. Before approving the transaction, the board’s investment committee demanded a comprehensive synergy sensitivity analysis. The corporate development team built a model that specifically varied the cross-selling adoption rate and the sales cycle timeline.

The analysis revealed a critical vulnerability: if the integration of the sales forces took twelve months longer than planned, the transaction’s net present value would drop by 45%. Furthermore, if the customer adoption rate reached only half of the baseline projection, the transaction would fail to meet its hurdle rate entirely.

Armed with this data, the acquirer restructured its offer. They reduced the upfront cash consideration by $300 million and replaced it with a performance-based earn-out tied directly to verified cross-selling revenue milestones. The move successfully insulated the buyer from significant financial damage when the sales integration subsequently faced severe technical delays.

Case Scenario 2: The Cross-Border Industrial Merger and Regulatory Frictions

Two major manufacturing giants, one based in North America and the other in Western Europe, announced a cross-border merger of equals designed to achieve massive operational efficiencies. The deal team identified $250 million in annual cost synergies, primarily driven by consolidating global supply chains, optimizing manufacturing plants, and harmonizing regional distribution networks.

However, the global M&A environment introduced severe regulatory headwinds. Antitrust agencies in multiple jurisdictions initiated prolonged reviews of the transaction. The internal deal team had anticipated these challenges by embedding a comprehensive sensitivity analysis into their initial planning phases. They explicitly modeled extended regulatory approval timelines and the potential forced divestiture of profitable production facilities.

The strategic chain reaction of regulatory intervention demonstrates the value of this foresight. A prolonged antitrust review directly forces the deferral of planned plant closures. This deferral subsequently extends duplicative corporate overhead across both operating regions.

The sensitivity matrix demonstrated that every month of delay in closing the transaction would cost the combined entity $15 million in duplicative operational overhead. Because they had identified this risk early, the management teams did not panic when regulators extended the review process by nine months. The companies had already secured extended bridge financing and adjusted their integration timelines based on the downside cases in their sensitivity model. The transaction successfully closed without triggering liquidity constraints or disruptive covenant violations.

Case Scenario 3: The Healthcare Consumer Goods Carve-Out and Cost-to-Achieve Overruns

A global healthcare conglomerate agreed to carve out and sell its underperforming consumer health division to a prominent private equity sponsor for $2.5 billion. The sponsor’s investment thesis focused entirely on operational cost reduction. They planned to extract $80 million in annual savings by carving the target out from the parent company’s bloated corporate infrastructure and establishing a lean, standalone IT and administrative framework.

The deal team’s diligence professionals conducted a rigorous sensitivity analysis focusing specifically on the “cost to achieve” these operational savings. They modeled the potential inflation of IT migration costs, legal separation fees, and transition service agreement (TSA) extensions.

The sensitivity findings were alarming: the baseline model assumed it would cost $100 million in one-time expenses to achieve the $80 million in annual savings. However, the sensitivity analysis showed that if the IT migration exceeded its timeline by just six months, the required TSA payments to the seller would jump by 150%, completely erasing the first two years of projected cost savings.

Recognizing this high concentration of risk, the private equity sponsor refused to accept the seller’s standard transition agreement terms. They negotiated a fixed-price TSA with severe financial penalties for the seller if separation milestones were delayed due to parental infrastructure dependencies. This analytical foresight preserved the sponsor’s investment margin and ensured a profitable exit four years later.

Moving Beyond Spreadsheet Optimism

In the high-stakes arena of global corporate transactions, relying on static, best-case financial assumptions represents a form of strategic negligence. Synergies are never guaranteed; they are hard-won operational efficiencies that require flawless execution, cultural alignment, and favorable market conditions.

Synergy-case sensitivity analysis serves as the ultimate diagnostic tool to strip away spreadsheet optimism and reveal the true risk profile of an acquisition. By systematically testing the timing, magnitude, and costs of integration assumptions, corporate leaders gain the clarity required to walk away from destructive deals and confidently pursue genuinely value-creative transactions. Ultimately, exceptional dealmaking is defined not by the sheer volume of transactions completed, but by the disciplined management of risk exposure across the entire investment lifecycle.

How resilient is your current acquisition pipeline when subjected to a rigorous synergy stress test?

Leave a comment